Best Short-Term Investment Plans In India 2026: Where To Park Money Safely

Whenever we talk about investment options and assets under consideration, the talk revolves around the impact of compounding and the importance of keeping a long-term perspective for the market. It is completely true that equities, debt, and other forms of investments provide the best compounding effect when held for a long period of time. However, what if you are saving for a short-term goal? What are the investment options if you require your corpus after a year, 18 months or after two years?

This usually happens when you are planning a vacation, buying a gadget or building an emergency fund. Choosing the right short term investment plan is critical because there are various circumstances when you cannot keep your money parked in an instrument for a prolonged period.

Options like liquid investments in India, short term debt funds, and fixed deposits (short-term) are emerging as the preferred choices for conservative investors seeking flexibility without compromising on stability.

Also Read: Best Short-Term Investment Plans For 3 Months

Best Short-Term Investment Options In India

If you are looking for an investment horizon of 6-24 months, the most critical aspects while choosing an investment option will be capital preservation, liquidity, and reasonable returns. Here is the summary of the best short term investments India:

Investment Option | Typical Instruments | Risk Vs. Return Profile |

Liquid funds / liquid investments India | Debt & money-market securities with very short maturities (up to ~91 days) | Lowest interest-rate risk, very high liquidity; recent 1-yr returns ~6.5%–7% for top funds. |

Ultra-short duration funds | Debt instruments with Macaulay durations of ~3-6 months, higher than liquid funds. | Slightly higher risk than liquid funds, slightly higher returns: around 7%+ p.a. in some cases. |

Short term bonds / short term debt funds | Debt funds or bonds with maturities of 1-3 years (or short-duration funds) | Moderate risk, decent returns; less ideal if you must withdraw in <12 months because of interest-rate risk. Return can be between 8-9% but is subject to market interest rate movements. |

Fixed deposits short term / recurring deposits India | Bank FDs or recurring deposits with time horizons matching your goal | Very safe, predictable, but returns may lag the top debt funds (5-7%, depending on the category of FD opted for); less flexibility (premature withdrawal may incur a penalty). |

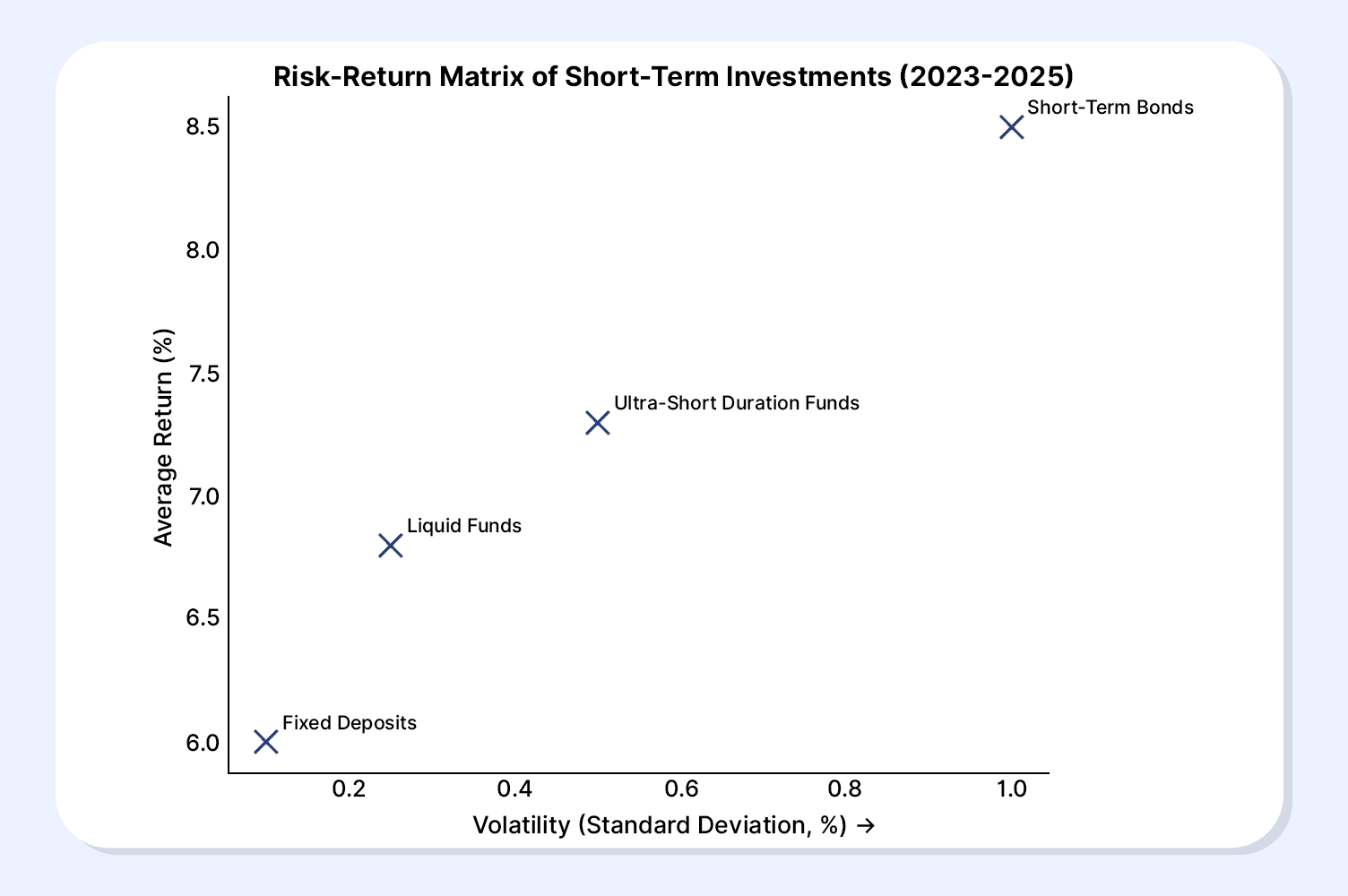

Here is the risk-return matrix of the short-term investment options:

Figure 1.0: Average Return vs. Risk (Represented by Standard Deviation of Returns, in %)

Why Bonds Are A Smart Choice

Compared to fixed deposits and liquid funds, bonds provide a comparatively higher return, even when the total risk (expressed as standard deviation) is not too high. Hence, bonds are often used as an investment option for attaining long-term investment goals. The ability of bonds to provide a moderate to high rate of return without too much risk makes them an excellent choice for short-term investment goals.

In 2025, bond yields in India remain attractive, with AAA-rated corporate bonds offering 7.5%-8.5% p.a., and short-term government securities around 6.8%-7.2% p.a.. These instruments can provide better inflation-adjusted returns than savings accounts, without exposing investors to significant volatility.

However, investors often have doubts about how to invest in bonds and whether these are as liquid as their equity-based investment counterparts. This is where platforms like Grip Invest come into play.

With Grip Invest, it is possible to invest in short-duration corporate bonds and Government of India Bonds through a transparent, fully digital process. Investors can select tenures as short as 6–18 months, track payouts online, and enjoy regular interest flows with minimal lock-in.

Taxation And Liquidity Comparison

Let us take into account the following table that considers two important factors: liquidity and post-tax returns of different alternatives for short-term investments:

Investment Type | Liquidity | Tax Treatment | Investment Tenure (Ideal) | Post Tax Return Potential |

Liquid Funds | T+1 redemption (usually within 24 hrs) | Taxed as per income slab, like STCG (since no LTCG benefit < 3 yrs) | 1-12 Months | ~5.0 – 5.5% (p.a.) considering tax for 30% slab |

Ultra Short Duration Funds | T+1 redemption | Taxed as per the income slab | 6-18 Months | ~5.3 – 6.0% |

Short-Term Bonds / Debt Funds | Moderate liquidity (may take 2–3 days) | Taxed as per slab (< 3 yrs) | 12-36 months | ~5.5 – 6.5% |

Fixed Deposits / Recurring Deposits | Premature withdrawal allowed (with penalty) | Interest fully taxable per slab | 6-24 months (can be longer, as per requirements) | ~4.5 – 5.5% |

The after-tax return potential is based on the highest slab rate of income tax @30%. For exact calculations, do consult your investment/tax advisor. Liquid and ultra-short duration funds offer the easiest redemption flexibility, while short-term bonds provide a slight edge in yield for those comfortable with a brief lock-in.

Conclusion

If you have short-term investment goals, there are a number of alternatives that you can choose from. You need not worry about compounding or double-digit ROI if your investment tenure does not exceed 2 years. Such investments are made for short-term goals such as buying an iPhone or taking a small vacation.

From liquid and ultra-short duration funds to short-term bonds and Treasury Bills India, the focus should be on aligning maturity with your goal timeline. Diversifying across instruments can optimise returns while managing risk, ensuring your money stays both accessible and productive throughout your short-term investment journey.

Visit Grip Invest today!

FAQs On Short Term Investment Plans In India

1. What is best for 1-year investment?

For a 1-year horizon, short-term bonds, liquid funds, or ultra-short-duration funds are ideal. They offer better returns than savings accounts, quick redemption (T+1), and minimal volatility, making them perfect for short-term goals.

2. Are short-term bonds better than FDs?

Yes, in many cases. Short-term bonds can deliver higher post-tax returns, especially when interest rates are stable or falling. However, FDs are preferable for investors seeking fixed, guaranteed income with zero market risk.

3. How to choose a short-term plan?

Start by defining your time horizon and liquidity needs. Then, match the product’s maturity and risk level accordingly: liquid funds for <1 year, short-duration bonds for 1–3 years, and FDs or T-bills if you prioritise safety over flexibility.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001