Best SIP for Short Term Goals in India 2026: Top Funds For 1–3 Year Horizons

Investors often use mutual fund SIPs to build long-term wealth. In 2026, SIPs can also support short-term financial needs. The best SIP for short-term 2026 may suit investors who want to park money with the potential to earn more than a regular savings account offering around 2 to 3 percent returns.

Short-term SIPs work differently from long-term equity SIPs.

The focus is usually on liquidity, lower volatility, and steady returns rather than aggressive growth. So, how do these SIPs work, who should consider them, and what should investors check before choosing one?

Let us explore.

What Is A Short-Term SIP?

Short-term generally means investment horizons of about one to three years. Under SEBI guidelines, short-duration funds have a duration ranging from 1 to 3 years. For even shorter time horizons, investors can use low-duration (6-12 months) or ultra-short-duration SIPs (3-6 months).

Recently, Union Mutual Fund introduced NFO for Union Low Duration Fund, which is targeting an investment duration of 3 to 12 months1.

| Investment horizon | Reader friendly meaning | Fund category to check |

| Below 6 months | Very short need where access to money matters most | Liquid Fund or Ultra Short Duration Fund SIP |

| 6 to 12 months | Near term goal where stability remains important | Ultra Short Duration Fund SIP, Low Duration Fund or Money Market Fund |

| 1 to 3 years | Medium short goal where investors may accept limited movement in returns | Short Duration Fund |

It is a practical reading aid. A one month expense needs a more cautious vehicle, while a three year target may allow a wider choice. Before investing, one should review exit load, credit quality, interest rate sensitivity, tax treatment and redemption timelines.

Who Should Invest In Short-Term SIPs?

Short-duration SIPs are appropriate for those who want disciplined, low-risk growth within a short period of time. They are best suited for financial objectives such as a down payment, wedding cost, or holiday savings. Experts also suggest that short-duration debt funds be used to park money set aside for emergencies in the face of stable interest rates. If you fall in the tax bracket above 20%, hybrid or arbitrage funds are more tax-efficient but with moderate risk2.

Goal-Based SIP Guide

Here is how different short term goals may be matched with suitable SIP options based on the time available and risk comfort.

| Financial need | Likely time frame | SIP option to consider | Why it may fit |

| Emergency fund | Up to 6 months | Liquid fund SIP | Offers quick access and aims to keep volatility low |

| Vacation planning | 1 to 2 years | Arbitrage fund or ultra short duration fund | Balances access, tax treatment and moderate return potential |

| Wedding expenses | 1 to 3 years | Ultra short duration fund or short duration fund | Suitable when the date is known and capital stability matters |

| Car or gadget down payment | 2 to 3 years | Conservative hybrid fund or short duration fund | Allows slightly wider choices, though risk should remain controlled |

Top Performing Short-Term SIP Funds In 2026

Debt-oriented SIPs invest in low-duration or short-duration debt mutual funds. They generally provide stable returns and carry a lower risk compared to equity mutual funds. So, they are well-suited for conservative, near-term objectives.

For instance, short-term debt funds may now be better than fixed deposits because fixed deposits yield maximum returns of up to 6% in the current rate scenario.

Equity-oriented SIPs, on the other hand, invest in equity funds, particularly mid-cap, infra, or PSU schemes. These may return high 1-year returns, typically in excess of 30%, but are accompanied by increased volatility. Due to the high risk involved with equity exposure for the short term, debt-oriented short-term SIPs are more preferred.

The following short duration funds have been shortlisted based on the visible April 2026 data. The filter used here is a 1-year return among the higher names in the category, along with AUM above INR 1,000 crore. This table on short-term SIP mutual funds in India is only for comparison.

Investors should also review portfolio quality, duration risk, exit load, expense ratio, taxation, and redemption timeline before investing.

Fund Name | Fund House | Fund Size (INR Cr) | 1 Y Return as of April 26 |

ICICI Prudential Short Term Fund | ICICI Prudential Mutual Fund | 20,688 | 6.16% |

Axis Short Duration Fund | Axis Mutual Fund | 8,342 | 5.91% |

Aditya Birla Sun Life Short Term Fund | 6,501 | 5.66% |

Source: INDmoney3

How To Start A Short Term SIP

The best SIP for short-term 2026 should begin with the purpose, not the scheme name. Decide how much you need, when the money may be used, and what level of fluctuation is acceptable. This makes the selection more disciplined.

1. Choose the financial need

Start with a clear requirement. It may be an emergency reserve, school fee, travel plan, wedding expense or down payment. A fixed timeline needs greater caution than a flexible one.

2. Review the minimum SIP amount

The entry amount differs across schemes and investment portals. Many mutual funds allow instalments from INR 100 or INR 500, while some require a higher contribution. Read the scheme document before registering.

3. Select a direct or regular plan

A direct plan is bought without a distributor and usually carries a lower expense ratio. A regular plan comes through an adviser or distributor. It may suit those who need assistance in choosing and monitoring the scheme.

4. Pick the contribution frequency

Monthly instalments work well for most salaried investors because they match income flow. Some portals may also offer weekly, daily or quarterly options. For near-term needs, monthly tracking is often easier.

5. Add the SIP end date

During registration, enter the start date, instalment value, frequency and final contribution date. Avoid an open-ended instruction when the target has a known timeline. A fixed stop date prevents unnecessary future deductions.

6. Manage auto debit carefully

The bank mandate allows automatic collection from the selected account. Keep an adequate balance before the deduction date to avoid failed payments. If the target amount is reached early, pause or stop the instruction through the AMC website, MF Central, RTA portal, or your investment app.

7. Review before withdrawal

Stopping the SIP only ends future instalments. It does not move the existing corpus to the bank account. Before withdrawing, review exit load, tax impact, current value and settlement time. For an upcoming payment, redeem early enough to avoid last-minute delays.

Now that the process is clear, the next step is to look at fund categories that may fit different short term needs.

Short-Term SIP Returns: What To Expect

Short term SIP returns should be viewed with caution. A one year period can be too brief for equity schemes because market swings may dominate the outcome.

This is why investors searching for the best SIP for 1 year in India may need to look beyond equity funds and assess categories with lower volatility.

For those comparing the best SIP for 3 years in India, the approach can be slightly wider, but risk still matters. In FY26, a recent analysis showed that 486 out of 556 schemes reviewed delivered negative SIP returns, with the weakest equity schemes falling sharply during the period.

The picture looked less severe in the one-year period ended April 2026, but volatility remained visible. Out of 286 equity mutual funds with a one-year record, only 27 delivered more than 10% SIP returns. Another 171 gave single-digit returns, 87 were negative, and one stayed flat.

Short-term SIPs, particularly in debt products, provide more stable but lower returns. Equity SIPs can perform better over a longer term, but for the short term, they can be volatile and even negative at times.

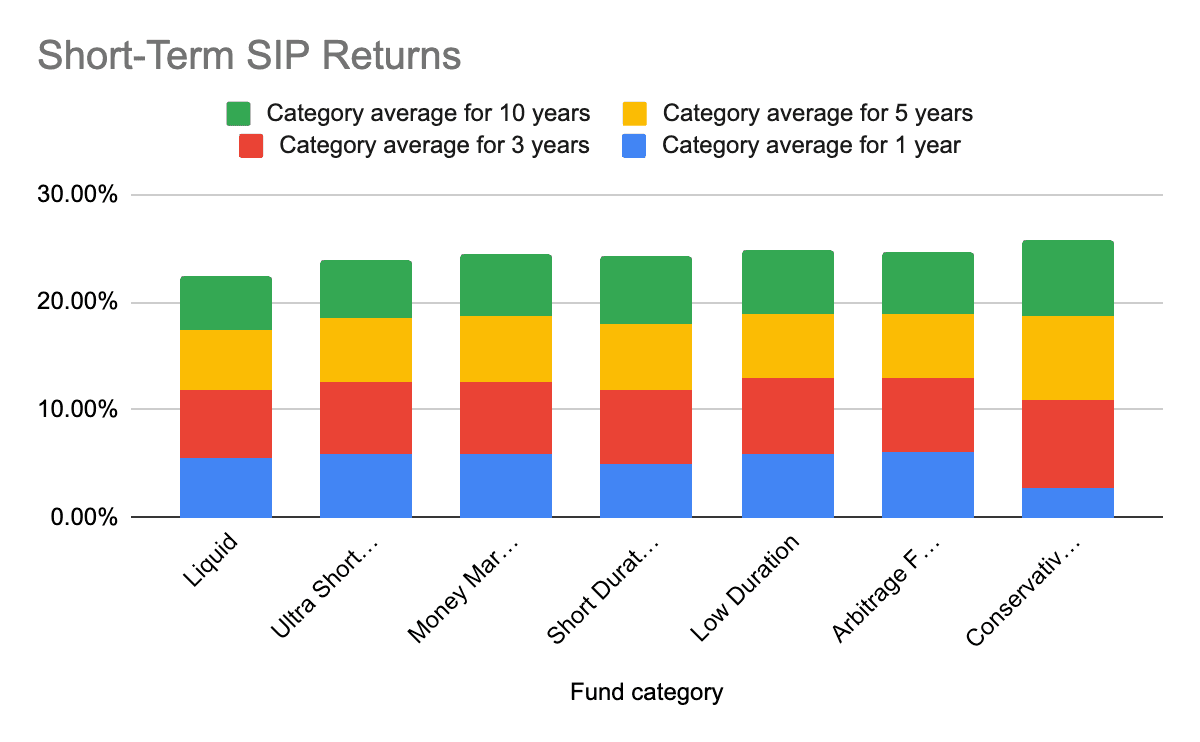

The chart below shows category average returns across different periods as of April 29, 2026, helping investors compare recent performance with longer term behaviour:

Source ET

The data shows that most debt oriented categories stayed broadly in the 5% to 7% range across these periods. Conservative Allocation delivered higher longer period averages, but it includes hybrid exposure and may carry more fluctuation than pure debt categories.

These are category averages, not assured returns. Investors should review scheme level risk, credit quality, exit load, tax treatment and redemption timelines before choosing a short term SIP.

Also Read: Know About The 8-4-3 Rule Of SIP

Key Factors To Choose The Best SIP For Short Term

Some of the important factors you must consider while choosing short-term SIPs are:

1. Expense Ratios And Liquidity

Expense ratios are the yearly charges charged by a fund house to pay for its overhead, management, administration, promotion, etc. Even low-looking expense ratios have a material impact on short-term gains, so it makes sense to choose funds with low expense ratios unless their performance merits paying more.

Higher liquidity funds, such as liquid or ultra-short duration debt funds, have quick redemptions with low market impact. These are suitable for short-term plans where the need to access cash is the priority.

2. Exit Load

Exit load is a charge levied if you sell the units before the given time. For short-term SIPs, little or no exit load is levied by several liquid and ultra-short-duration debt schemes. This is done to avoid very short-term churning and maintain stability in funds.

There is usually a graded exit load, for instance, a levy of approximately 0.007% on day 1, which declines on a daily basis until it becomes zero from day 7.

3. Taxation

Taxation varies with fund category and holding period

- Equity oriented funds are generally taxed under the equity mutual fund framework. For units transferred on or after 23 July 2024, short term capital gains on equity oriented funds are taxed at 20% if the holding period is 12 months or less. Applicable surcharge and cess may also apply.

- Debt oriented mutual funds need a more careful reading. For specified mutual funds acquired on or after 1 April 2023, gains are treated as short term capital gains and taxed as per the investor’s income tax slab. It mainly covers funds investing more than 65% in debt and money market instruments, along with certain fund of funds.

Also Read: (New) Tax Rules For Debt Mutual Funds In 2026 – What Every Investor Must Know

Conclusion

Short-term SIPs in debt funds are suitable for those requiring capital in less than three years. They have lower risk compared to equity, offer simpler capital preservation, and provide stable returns. Investors who need funds in the short term and prioritise accessibility over returns can invest in short-term SIPs.

Following the RBI's hold on repo rates, experts continue to favour short-duration debt funds for short-term needs and emergency savings. Grip Invest offers many short-term debt mutual fund options for investors seeking clarity, lower risk, and time-bound returns. To invest in a short-term SIP, consider signing up on Grip Invest today.

Frequently Asked Questions On Short-Term SIPs

1. Which SIP is best for 1 year?

Ultra-short and short-term debt funds can be a good option for one-year SIPs. These provide stable returns with low risk (compared to equity) and high liquidity. You can explore multiple short-term debt funds on Grip Invest from leading AMCs like Nippon India, Axis Bank, ICICI Prudential and HDFC. Please note that these debt funds also come with certain risks, and hence, investors are advised to read the offer-related documents carefully before investing in any debt instrument.

2. Is SIP good for short-term investments?

Yes, if you choose debt-oriented SIPs. They combine predictability with income potential. Equity SIPs can give high long-term returns, but for short time frames, they tend to give negative results. More than 50 equity SIPs lost money in the last year. So, SIP can be good for short-term investments if the SIP is done in debt mutual funds after carefully analysing the mutual fund scheme.

3. What are the risks of short-term SIP?

Debt funds, especially low-duration ones, can fluctuate if interest rates change. While not common, they may cause short-term redemption difficulty or small erosion of capital. If short-term SIP is being done in equity mutual funds, then there is a high risk of negative returns, too.

4. How are SIP returns taxed when I redeem after only 1 year?

Each SIP instalment is taxed based on its own holding period. After one year, equity oriented funds may face equity capital gains tax, while specified debt funds are generally taxed as per the investor’s slab rate.

5. Is an arbitrage fund better than a liquid fund for short-term SIP goals?

It depends on the holding period, tax bracket and need for quick access. Arbitrage schemes may suit slightly longer timelines, while liquid options are often preferred when stability and faster redemption matter more.

References:

- The Economic Times, accessed from: https://economictimes.indiatimes.com/mf/mf-news/nfo-alert-union-mutual-fund-launches-low-duration-fund/articleshow/122089580.cms

- The Economic Times, accessed from: https://economictimes.indiatimes.com/mf/analysis/rbi-mpc-what-strategy-should-debt-mutual-fund-investors-follow/articleshow/123138190.cms

- IND Money, accessed from: https://www.indmoney.com/mutual-funds/debt/short-duration

- The Economic Times, accessed from: https://economictimes.indiatimes.com/mf/analysis/up-to-34-crash-sip-investors-suffer-double-digit-loss-in-130-equity-mutual-funds-in-fy25/articleshow/119291389.cms?from=mdr

- Market Insights India, accessed from: https://marketinsightsindia.in/sip-returns-over-the-years-a-historical-view-for-indian-investors/

- Aditya Birla Capital, accessed from: https://www.adityabirlacapital.com/abcd/mutual-funds/debt-funds/ultra-short-duration-funds

- The Economic Times, accessed from: https://economictimes.indiatimes.com/mf/analysis/over-50-mutual-fund-sips-give-negative-returns-in-1-year-should-you-pause-redeem-or-continue/articleshow/123180260.cms

- Association of Mutual Funds of India, accessed from: https://www.amfiindia.com/investor-corner/knowledge-center/tax-corner.html

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001