Debt Equity Swap Explained: Portfolio Rebalancing Guide India 2026

Introduction To Debt Equity Swap

Imagine you are at a party where everyone is buzzing about the next big stock tip, but the real winners? They are quietly sipping their drinks, sticking to a plan that outlasts the hype. That is debt equity swap in action, a game-changer in disciplined asset allocation where you pivot from safe-haven debt like bonds to high-octane equities, keeping your portfolio’s risk in check amid life’s financial rollercoasters1. it is not about chasing unicorns; it is restoring balance when markets pull your allocations off-course, aligning every rupee with your dreams, be it retirement or kids’ education.?

Fast-forward to India’s bustling markets: Post-2025 reforms, Nifty’s wild swings have left many portfolios lopsided, with equities devouring debt shares. Regular debt equity swaps act as your financial GPS, preventing overexposure that could wipe out gains in a downturn2. This sets the perfect stage to dive deeper: What exactly is this swap, and how does it work its magic? Let us unpack it next, building on why allocation trumps timing every time.

What Is A Debt Equity Swap?

Now that we have seen why asset allocation is your portfolio’s North Star, let us get hands-on with debt equity swap,the tactical move that keeps you on track. Imagine selling off those cozy fixed-income stars like FDs or debt mutual funds, then channeling the cash into equities to nail your ideal mix, say 60:40 equity-debt3. it is worlds apart from corporate drama under IBC, where banks swap loans for shares in distress; here, it is your personal power play in India is booming INR 50 lakh crore mutual fund arena, demanding discipline over drama.

Take a real-world example. You start with a ?20 lakh portfolio split evenly between equity and debt. A strong bull run pushes equities up to 65%, throwing the balance off. To rebalance, you shift around ?3 lakh from equity back into debt, restoring the original allocation.

This is not a clunky process. Investors often use ultra-short debt funds for this purpose,they offer reasonable yields of around 6.5–7% with high liquidity, making it easier to move money into equities later without long cash idle periods.

These mechanics lead to the more important question: when should you actually rebalance? That decision depends less on exact numbers and more on market conditions,something we will explore next.

When Does A Debt-To-Equity Swap Make Sense?

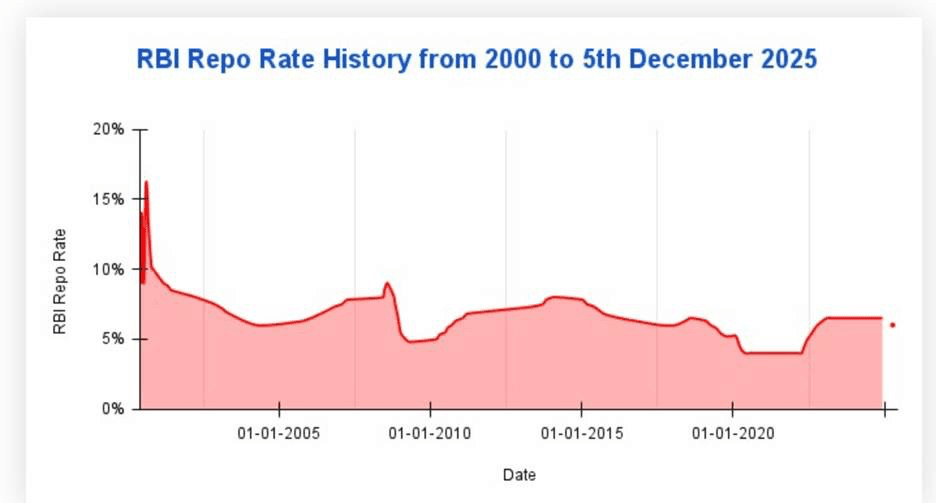

Knowing the swap's structure reveals prime windows: execute debt to equity shifts during corrections when Nifty P/E dips below 22x, capturing undervalued growth. Falling RBI rates-slashed to 5.75% by late 2025-favor equities as borrowing costs drop, lifting midcaps 20% annually, unlike rising rate eras favoring 8% FD yields4. The 5/25 rule guides: rebalance at 5% deviation or 25% total drift, reducing volatility by 25-35% per Vanguard studies adapted for India.

Source: basu nivesh5

Hypothetical: INR 10 lakh at 60:40 grows equities 25% to INR 7.5 lakh (75%); swap INR 1.5 lakh debt-to-equity restores balance, yielding 12% CAGR vs. 9% unchecked. These triggers naturally lead to weighing tax and return trade-offs in execution.

Tax And Return Impact Of Debt Equity Swaps

Timing swaps profitably hinges on tax efficiency, as equity LTCG over INR 1.25 lakh taxes at 12.5% post-1 year, while debt under 24 months hits slab rates up to 30%5. Post-2023 rules, debt LTCG is 12.5% sans indexation, making >3 year holds ideal for portfolio rebalancing. Consider this table for clarity:

| Scenario | Period | Equity Tax | Debt Tax | Return Boost (INR 10L, 5 yrs) |

| Debt to Equity Swap | >1 yr | 12.5% LTCG | N/A | +18% (bull phase) |

| Equity to Debt | <2 yrs | N/A | 30% slab | Risk cut 40%, +2% alpha |

| Quarterly Rebalance | Mixed | 8-10% avg | 15-20% | 11.8% vs 10% buy-hold |

Source: clear tax7

Rebalanced portfolios averaged 12.2% CAGR (2015-2025), outpacing benchmarks by 1.5%, but taxes erode 1-2% annually,prompting smart execution strategies next.

How To Execute Debt Equity Swaps Smartly

Tax-aware timing flows into practical steps, turning strategy into action for seamless debt equity swaps. Start with low-cost mutual funds and ETFs: Sell liquid funds at just 0.15% expense ratios, then pivot proceeds into Nifty Bees for instant equity exposure without brokerage bites. This keeps costs under 0.3% annually, preserving your hard-earned returns amid India's competitive MF landscape.

Automate the magic with balanced advantage funds,they dynamically tilt debt to equity shifts based on valuations, curbing emotional trades during 2025's brutal 15% corrections that tested even pros. Picture this: No more FOMO sells; the fund handles rebalancing, targeting 65:35 ratios with 13% uptrend yields.

Anchor your moves in stable debt like AAA corporate bonds or Bharat Bond ETFs yielding 7.2%, providing predictable ballast against equity storms. Your foolproof playbook unfolds in four steps:

- Scan and calculate: Use MF Central or Excel to spot drifts,formula: (Current% - Target%) × Portfolio value = Swap size.

- Execute tax-smart: Opt for same-AMC switches to defer capital gains hits.

- Diversify smartly: Mix large-cap ETFs (60%) with midcaps (20%) for balanced growth.

- Review rhythmically: Quarterly checks align with market cycles, flowing straight into FAQs for real-world tweaks.

Newbies thrive here,apps like Kuvera send drift alerts, making portfolio rebalancing child's play. This precision not only boosts 1-2% alpha but bridges perfectly to addressing common doubts. What exactly is the execution roadmap-

Execution roadmap:

- Track via MF Central: Input holdings for drift alerts.

- Compute: (Actual% - Target%) x Total value = Swap size.

- Switch in-house (same AMC) to defer taxes.

- Review quarterly, linking to FAQs for beginners.

Hybrid funds simplify for novices, auto-rebalancing 65:35, yielding 13% in uptrends. This precision addresses common doubts raised next.

Conclusion

Debt equity swaps are less about chasing returns and more about staying disciplined through market cycles. By rebalancing at the right time, investors can control risk, improve long-term outcomes, and keep their portfolios aligned with real financial goals. Platforms like Grip Invest make this process easier by helping investors understand asset allocation, market cycles, and smarter portfolio decisions, so investing stays structured even when markets are not

Frequently Asked Questions

1. Is a debt equity swap suitable for long-term investors?

Yes. It works best for long-term investors who want to maintain their target asset allocation and reduce risk without trying to predict market highs and lows.

2. Does a debt equity swap always trigger tax liability?

Tax applies when you redeem units, but equity gains after one year are taxed at a lower rate, and some in-house mutual fund switches can help manage tax impact efficiently.

3. How often should an investor consider rebalancing using debt equity swaps?

Most investors rebalance annually or when allocations drift by 5–10%, while more volatile markets may require more frequent reviews.

References:

1. Bajaj finserv, accessed from: https://www.bajajfinserv.in/investments/what-is-portfolio-rebalancing

2. Master trust, accessed from:

https://www.mastertrust.co.in/blog/portfolio-rebalancing-today

3. Bajaj finserv, accessed from: https://www.bajajfinserv.in/debtequity-swap

4. Share india, accessed from: https://www.shareindia.com/knowledge-center/share-market/are-you-rebalancing-your-portfolio-why-and-how-to-do-it

5. basu nivesh, accessed from: https://www.basunivesh.com/rbi-repo-rate-history-from-2000/

6. Economic times, accessed from: https://economictimes.indiatimes.com/wealth/tax/will-switching-from-equity-to-debt-schemes-of-the-same-fund-house-have-tax-implications/articleshow/65080347.cms

7. Clear tax, accessed from: https://cleartax.in/s/tax-on-debt-funds

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001