Diluted EPS: Meaning, Calculation, And Why Investors Should Care

Want deeper insights into your organisation’s financial health and performance? Diluted EPS, also known as diluted earnings per share, is an important measure for this. It helps to decide the amount of profit a company will gain from each share of stock. Determining the profitability of a stock becomes a possibility through this.

To understand more about its meaning, ways to calculate and benefits for investors, continue reading further.

This blog is a complete guide to understanding everything about Diluted Earnings Per Share.

What Is Diluted EPS?

The simplest way to think about Diluted EPS is that it is what each share of a company would earn if every possible new share were already in circulation. Companies do not just have the shares you see trading on the stock exchange. They also have obligations, stock options handed to employees, convertible bonds that can be flipped into equity, and warrants issued to early investors.

None of these are shares yet. But they could become shares. And when they do, your slice of the earnings pie gets smaller. Diluted EPS assumes all of that has already happened. It's a worst-case and more realistic look at per-share earnings.

Diluted EPS formula is:

Diluted EPS = Adjusted Net Income ÷ (Weighted Average Shares + All Dilutive Potential Shares)

How Is It different From Basic EPS?

Basic EPS is straightforward: net income divided by shares currently outstanding. And this is not a criticism, basic EPS has its own uses. It is clean, quick, and easy to track quarter over quarter.

However, the only drawback is that it leaves out an enormous amount of information, particularly for companies that compensate employees heavily through stock options or have raised money through convertible instruments.

Consider a hypothetical example: a company reports basic EPS of INR 12. Looks decent. But the company also has employee stock options outstanding that, if exercised, would add 30% more shares to the pool. Suddenly, that INR 12 becomes something closer to INR 9 on a diluted basis.

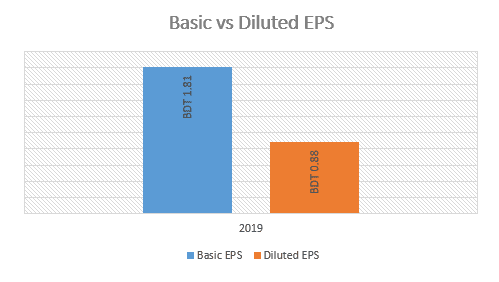

Hence, between Basic EPS vs Diluted EPS, the latter will be used by anyone and everyone to build their investment thesis and decisions upon.

Source: PWC1

How Diluted EPS Is Calculated?

The mechanics involving diluted earnings per share calculation involve two separate methods, depending on what kind of dilutive security you are dealing with.

Both methods seem logical and intuitive once the reasoning behind them is understood.

1. Convertible Securities: If-Converted Method

Convertible bonds can be exchanged for equity shares at some future point. The if-converted method assumes that exchange has already happened.

Two things shift simultaneously in this. The share count increases because new equity now exists. But net income also nudges upward, because if the debt has been "converted," the company is no longer paying interest on it. You add back that interest expense (adjusted for tax) to the numerator.

Whether this conversion is included in the final fully diluted share figures depends on whether it actually lowers EPS. If the math works out to raise EPS instead, it's classified as antidilutive and left out. Only genuinely dilutive conversions are counted.

2. Stock Options: The Treasury Stock Method

Stock options do not work the same way. Here, the assumption is that in-the-money options get exercised, and employees pay the strike price to receive shares.

The company then takes that cash and uses it to buy back shares at the current market price.

The net new shares (exercised minus bought back) are what hit the diluted share count. It is not the full options pool, just the difference.

This keeps the dilution figure realistic rather than alarmist. Out-of-the-money options are excluded entirely. Nobody exercises an option that costs more than the stock is worth.

Why Diluted EPS Matters?

Diluted EPS matters because of its various advantages for any investor. It gives a realistic view of the earnings and has an honest impact on the valuations.

1. Cleaner Picture of the Earnings

Stock-based compensation is a real cost to shareholder value over time. Diluted EPS captures this cost in a way basic EPS never does. This matters most in sectors where equity compensation is structural, like tech startups, early-stage pharmas, etc.

A company might show impressive basic EPS growth while quietly expanding its options pool every year.

Investors tracking only basic EPS miss the slow erosion happening underneath.

2. Makes Valuations more Honest and Reliable

The price-to-earnings ratio is only as reliable as the EPS method used to calculate it. While the basic EPS just gives an optimistic price-to-earnings ratio, using diluted EPS interpretations changes the entire picture for investors.

Say a stock trades at INR 600. Basic EPS is INR 30, giving a P/E of 20x, which looks reasonable. Diluted EPS comes in at INR 21. That P/E is now 28.5x. Same stock and same price, but an entirely different valuation story is reflected through both.

Analysts who build serious models always use diluted figures for exactly this reason.

Limitations Of EPS Metrics

Despite being a more rigorous method than Basic EPS, Dilute EPS still has its own shortcomings and limitations.

1. Has Flaws of Net Income

Diluted EPS is only as reliable as the net income figure it starts from. Net income is shaped by accounting choices, how assets are depreciated, when revenue is recognised, and how extraordinary charges are classified. Diluted EPS does nothing to correct for this; it simply passes those distortions through.

2. Anti-Dilutive Securities Remain Invisible

Instruments that would increase EPS upon conversion are excluded from the diluted calculation by definition. An antidilutive security today can become dilutive after a price correction. Investors reading diluted EPS get no warning of this latent exposure sitting just off the reported figures.

Conclusion

Diluted EPS exists because companies do not only have the shares that trade today, but they also have the shares they have promised. Treating those promises as irrelevant until they materialise is how investors end up surprised by the dilution they could have seen coming.

The best use of it is to use it as a valuation input and management tracking tool. Want to invest where the return is stated before you put the money in, no earnings calls and no dilution risk. Explore Grip Invest, a SEBI-regulated platform offering corporate bonds, to know more about this.

FAQs

1. What is diluted EPS?

Diluted EPS measures earnings per share after accounting for all securities that could convert into common stock, options, warrants, convertible bonds, and preference shares. It gives a more complete picture of per-share profitability than basic EPS by reflecting the full scope of a company's share obligations.

2. Why is diluted EPS lower than basic EPS?

Adding potential shares to the denominator spreads the same earnings across a larger base, which reduces the per-share figure. The only exception is antidilutive instruments. These are excluded because including them would push EPS artificially higher.

3. How do companies calculate diluted EPS?

Convertible securities are handled using the if-converted method: assume conversion has occurred, add the resulting shares to the count, and add back any related interest expense to net income. Options and warrants use the treasury stock method: assume exercise, model a market-price buyback using the proceeds, and count only the net new shares. Securities that fail to reduce EPS are left out of the calculation entirely.

References:

1. PWC, accessed from: https://tinyurl.com/2rkvbx3a

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001