EGR vs SGB: Which Gold Investment Is More Tax Efficient In India?

There are numerous considerations based on which an investment decision is made. While making an informed decision, comparing the returns on investment should be a fundamental criterion.

However, investors, especially the young ones, often overlook the importance of factoring in other considerations, such as post-tax returns on investment, which can significantly reduce an investor's actual benefits.

Let us suppose you have INR 1,00,000/- (rupees one lakh) to invest, and there are two options offering 8% and 9% returns, respectively (with similar levels of risk and underlying assets). Naturally, you will be inclined to invest in the latter. However, suppose the applicable tax rate on the first alternative is 12.5%, whereas the second option is taxed at 30%, now you will have to factor in the post-tax returns.

For gold based investments: EGR (Electronic Gold Receipt) and SGB (Sovereign Gold Bonds), the pros and cons (of investing) might have some commonalities.

However, the eventual investment decision should be made based on the tax efficiency of these alternatives. Let us find out more.

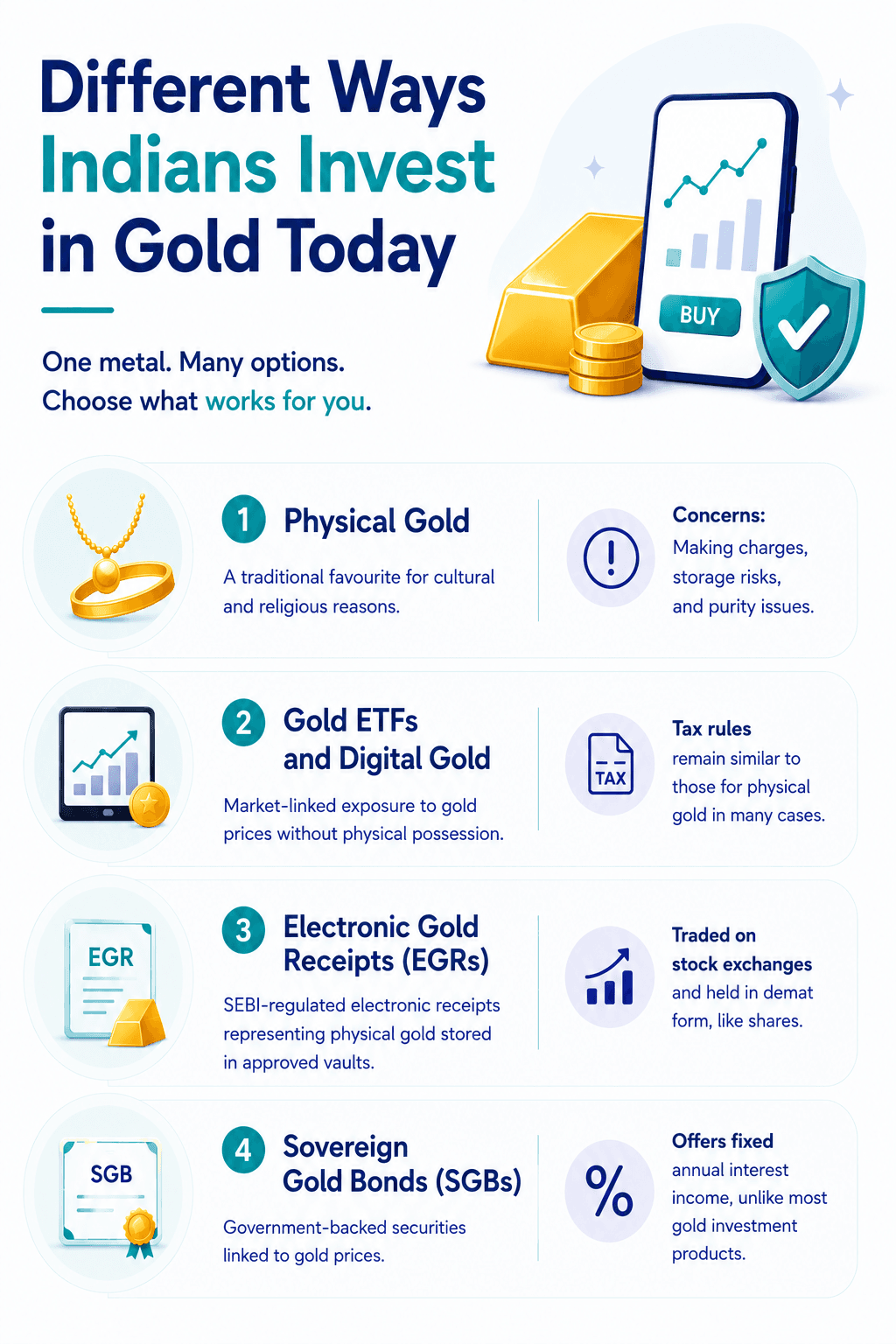

Different Ways Indians Invest In Gold Today

1. Physical Gold

The discussions around purchasing physical gold were sparked a bit when the PM appealed to citizens to refrain from buying gold, at least for a year. However, for cultural and religious reasons, physical gold remains one of the most preferred investment options in the yellow metal. There are some concerns, such as making charges, storage risks, and purity issues, which are addressed by digital and electronic alternatives.

2. Gold ETFs and Digital Gold

Gold ETFs and digital gold platforms offer market-linked exposure to gold prices without requiring physical possession. These products are easier to buy and sell, though tax rules remain similar to those for physical gold in many cases.

3. Electronic Gold Receipts (EGRs)

An electronic gold receipt vs sovereign gold bond comparison often starts with understanding what EGRs are. EGRs are SEBI-regulated electronic receipts representing physical gold stored in approved vaults. They are traded on stock exchanges and held in demat form, similar to shares.

4. Sovereign Gold Bonds (SGBs)

SGBs are government-backed securities issued by the Reserve Bank of India on behalf of the Government of India. These bonds are linked to gold prices and additionally offer fixed annual interest income, making them different from most gold investment products.

EGR vs SGB: Key Differences

Before diving into the specifics about the tax treatment of the two alternatives, let us understand the most critical differences between the two:

Parameter | EGR | SGB |

Issuer | SEBI regulated exchanges | RBI on behalf of the Government of India |

Underlying Asset | Physical gold stored in vaults | Gold-linked government security |

Returns Structure | Depends on the gold price movement | Gold price appreciation + fixed interest |

Interest Income | No interest payout | 2.5% annual interest |

Liquidity | Exchange traded with relatively higher liquidity | Tradable, but liquidity may vary |

Lock-in Period | No mandatory lock-in | 8-year tenure with an exit option after 5 years |

Redemption | Can convert into physical gold | Redeemed in cash equivalent |

Market-Linked Pricing | Yes | Yes |

Ideal Investor | Traders and flexible investors | Long-term investors |

The table above shows all the major differences between EGR and SGB, except for taxation. The discussion around SGB vs EGR taxation becomes important because both products may track gold prices similarly, but their post-tax returns can differ substantially over longer holding periods. Let us now move towards the business end of our discussion.

Tax Benefits And Investment Returns

- Tax Benefits of SGBs

Sovereign Gold Bonds offer a wide range of tax benefits to the investors. The 2.5% guaranteed coupon per annum is chargeable to tax under the other sources category, as per the applicable tax slab. However, if the investor holds SGBs throughout its tenure, the maturity amount (capital gains) is exempted from tax.

However, if the investor does not hold the SGBs throughout the tenure, no indexation benefits are available on the capital gain. Capital gains will be taxable at 12.5% without indexation for long-term holdings, or at the slab rate for short-term holdings.1

Also Read On SGB Taxation in 2026

- Tax Treatment of EGRs

The tax treatment of EGRs is quite similar to that of gold mutual funds or ETFs (or any listed security). If it is sold within 12 months, short-term capital gains will be taxed at the investor’s slab rate. On the other hand, if the holding period exceeds 12 months, long-term capital gains at 12.5% apply without indexation benefits.

If you have not redeemed your EGRs but converted them into physical gold, no capital gains tax is applicable.

Note: For the exact tax calculation depending on your investments (SGBs or EGRs), we strongly recommend that you consult your tax advisor.

Return Comparison Perspective

From a post-tax perspective, SGBs may deliver stronger long-term returns because they combine gold price appreciation, fixed interest income, and tax efficiency (as capital gains tax can be fully exempt when SGBs are held until maturity). EGRs, meanwhile, may appeal more to investors prioritising liquidity and active trading flexibility.

Which Is Better For Different Investors?

1. Long-Term Investors

For investors willing to hold the assets until maturity, SGBs not only offer consistent income (in the form of guaranteed coupons) but also provide capital gains tax exemption. The investment can be particularly suitable for wealth preservation goals.

2. Traders and Active Investors

EGRs may suit traders and short-term investors better due to their exchange-traded nature and relatively easier liquidity. Investors can enter and exit positions more flexibly without long lock-in periods.

3. Passive Investors

Passive investors looking for government-backed exposure to gold prices may find SGBs attractive. The fixed-interest payout adds a layer of predictable returns alongside gold's appreciation potential.

4. Investors Seeking Diversification

A proper gold investment comparison with India investors should also include diversification needs. While gold can help hedge against inflation and uncertainty, combining gold exposure with diversified fixed-income investments may help create a more balanced portfolio with stability and predictable income generation.

Conclusion

Both alternatives (SGBs and EGRs) are excellent investment options, especially when you are looking to diversify your portfolio with exposure to gold without assuming the risks associated with physical gold. The right choice ultimately depends on an investor’s time horizon, liquidity preference, taxation considerations, and overall portfolio strategy.

Since tax efficiency should be a major concern when making an informed decision, SGBs are well-suited to the needs of long-term investors, whereas for traders and short-term investors, EGRs might just do the trick.

Grip offers corporate bonds and other fixed-income investment options with yields up to 12.5% and institutional-grade security features. Visit Grip Today!

FAQs On EGR vs SGB

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001