Flexi FD: How It Works, Benefits, Features And Who Should Choose It?

A large savings balance feels safe because it remains available for bills, transfers and emergencies. However, the money often remains underutilised and earns a lower interest rate.

For example, as of 15 July 2026, SBI pays 2.5% a year on savings accounts, while its retail deposits for 1-2 years pay 6.25% to the general public.1,2 On INR 1 lakh held for one year, choosing the fixed deposit over a savings account earns you an extra INR 3,750 (before taxes).

However, a regular FD also involves a trade-off. Because the depositor may need to close the FD prematurely when an unexpected expense arises. Premature closure may reduce the applicable interest rate and, in some cases, trigger a penalty, lowering the final return.

A Flexi fixed deposit, or Flexi FD, addresses this gap between liquidity and interest income. It keeps a specified amount available in the savings account and automatically transfers the excess into linked term deposits. When the savings balance cannot cover a payment or withdrawal, the bank moves the required amount back from the deposit.

This arrangement may sound simple, but the way it works can vary widely across banks. The following sections explain how money moves, who may benefit and how a flexi fixed deposit compares with a regular FD.

How Money Moves Between Savings And Flexi FD?

The following flow shows what usually happens after income reaches the linked account.

1. Money moves from savings to the FD

The process begins when the savings account balance crosses a threshold fixed by the bank. It retains the required balance and automatically transfers the eligible surplus into one or more linked fixed deposits.

For example, suppose the threshold is INR 25,000 and the balance rises to INR 1 lakh. The bank may retain INR 25,000 in the savings account and move the remaining INR 75,000 into linked deposits.

This movement is generally called a sweep-out or auto sweep FD. Banks may create deposits in specified blocks rather than moving every rupee separately. IDFC FIRST Bank, for instance, creates 370-day FDs in INR 1,000 multiples when the savings balance exceeds INR 50,000.3

The transferred amount then earns the interest rate applicable to the linked FD. However, the actual earnings depend on how long each deposit remains invested.

2. Money returns when the savings balance falls short

The reverse movement begins when the savings account does not hold enough money to complete a withdrawal, transfer or payment. The bank then breaks part of the linked deposit to cover the shortfall.

This process is called a sweep-in FD or reverse sweep. The bank may transfer the exact deficit or break deposits in fixed units, depending on its product rules.

For example, SBI Savings Plus processes reverse sweeps in INR 5,000 units.4 Therefore, a shortfall of INR 12,000 may require the bank to reverse INR 15,000 from the linked deposits.

IDFC FIRST Bank follows a different structure. Although it creates FDs in INR 1,000 multiples, it permits sweep-ins in INR 1 units. This allows the bank to break only the amount needed to maintain the required savings balance.

The remaining deposit continues earning interest. The withdrawn portion generally earns interest for the completed holding period, subject to the bank’s premature-withdrawal policy.

Which deposit does the bank break first?

When several linked deposits exist, the bank may use one of two withdrawal methods:

- LIFO or Last-in, First-out: The newest deposit is broken first, allowing older deposits to continue towards maturity.

- FIFO or First-in, First-out: The oldest deposit is broken first, even if it has accumulated interest for a longer period.

Banks do not follow one universal structure. Flexi deposit rules vary across banks and even between account variants offered by the same bank. HDFC Bank, for example, currently sets sweep-out thresholds ranging from INR 35,000 for its Kids Advantage Account to INR 1.25 lakh for SavingsMax. The balance retained in the savings account ranges from INR 25,000 to INR 1 lakh across these variants.5

Therefore, before activating an auto sweep FD, account holders should check the threshold, deposit block size, withdrawal order and premature-interest rules.

What Should You Check Before Activating a Flexi FD?

Although a Flexi FD automates cash management, its features vary across banks. Before enabling the facility, compare the following aspects carefully.

| Factor | Why it matters |

| Sweep-out threshold | Determines the balance level in your savings account above which surplus funds are automatically moved to an FD; affects liquidity and how much idle cash earns higher interest. |

| Deposit block size | Some banks create FDs in fixed multiples (e.g., ?1,000, ?10,000) while others allow flexible amounts; influences whether the full surplus can be parked or only rounded chunks. |

| Sweep-in rules | Define how the bank brings money back from the FD to the savings account (only required amount vs. breaking whole FD units); impacts how much principal/interest is accessed and any interest recalculation. |

| Premature withdrawal policy | Banks may reduce interest on the withdrawn portion or charge a penalty when breaking an FD; affects the effective return and cost of using sweep facilities for short-term needs. |

| Minimum balance requirement | You must leave enough in the savings account for routine transactions and auto-debits; if sweep rules ignore this, you could face penalties or failed payments. |

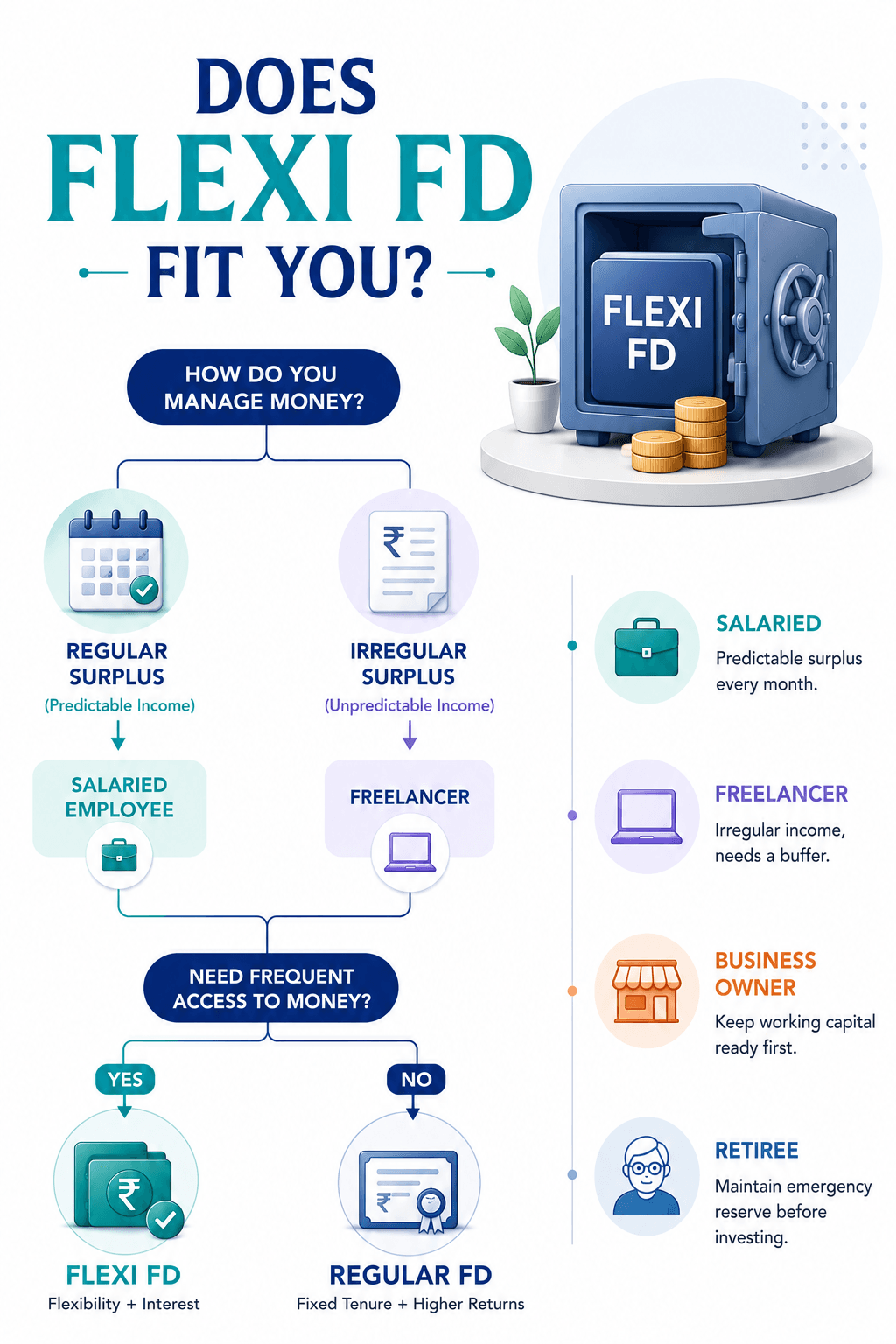

Does Flexi FD Suit Your Lifestyle?

Suitability depends on how regularly money enters the account and how often the surplus may be needed again.

1. Salaried employee

A salaried employee may find the facility useful when monthly income leaves a predictable surplus after rent, EMIs, bills and routine expenses.

Instead of leaving that surplus in the savings account, the auto sweep can move it into linked deposits. However, the employee should retain enough money for upcoming payments so that frequent withdrawals do not repeatedly break the FD.

2. Freelancer

A freelancer may receive large payments at irregular intervals, followed by weeks or months with lower income. A Flexi FD can help move temporary surplus into a deposit while keeping it connected to the savings account.

The main risk is overestimating how much money is truly spare. Freelancers may need a larger savings buffer for taxes, project delays and low-income periods, as repeated sweep-ins can reduce interest earnings.

3. Business owner

A business owner may use an auto-sweep facility to manage temporary cash that is not immediately required for salaries, supplier payments or working capital.

However, business cash flows can change quickly. The account holder should check whether the facility is available on the relevant current account, how quickly funds return and whether withdrawals happen in fixed blocks.

Operating money should not be treated as long-term surplus. A missed payment can cost more than the additional interest earned.

4. Retiree

A retiree may value the combination of access and interest, particularly when part of the savings must remain available for medical expenses or household needs.

However, a Flexi FD may not provide the same predictability as a regular FD with scheduled interest payouts. Retirees should first estimate their monthly income needs and emergency reserve before moving surplus money into an automated deposit.

A Flexi FD may suit people who want flexibility without manually opening deposits each time. However, those with a clear investment period and limited need for withdrawals may find a regular FD more suitable, as the next comparison explains.

When Might A Flexi FD Not Be Suitable?

A Flexi FD may not be the right choice for everyone.

It may be less suitable for investors who:

- Already know exactly how long they can invest their money.

- Prefer a regular fixed deposit with a defined maturity amount.

- Frequently withdraw almost their entire account balance.

- Maintain only a small savings balance that rarely exceeds the sweep threshold.

In these situations, a traditional fixed deposit or another fixed-income investment may better match the investor's requirements.

Common Mistakes To Avoid When Using a Flexi FD

A Flexi FD can improve returns on idle cash, but only when it is used appropriately. Some common mistakes include:

- Setting the sweep threshold too low and leaving insufficient funds for regular expenses.

- Treating emergency savings as long-term surplus.

- Ignoring the bank's premature withdrawal rules before activating the facility.

- Assuming all banks offer identical sweep-in and sweep-out features.

- Choosing a Flexi FD without comparing the linked fixed deposit interest rate with other available options.

Reviewing these aspects before activation can help investors use the facility more effectively.

Flexi FD Versus Traditional FD

Both products use term deposits, but they solve different cash-management needs.

Factor | Flexi FD | Regular FD |

Liquidity | Automatic partial or block-wise reverse sweep | Usually requires a premature-closure request |

Returns | Depends on swept amount, completed tenure and breakage rules | Contracted rate applies when held to maturity |

Convenience | Surplus moves automatically after activation | Amount, tenure and renewal are selected manually |

Minimum balance | Linked-account threshold varies by bank | Minimum opening deposit varies by bank |

Auto sweep | Included in the arrangement | Usually unavailable unless separately linked |

Best suited for | Short-term surplus with uncertain timing | Money available for a known period |

An important difference is that regular FD usually gives investors greater control over the investment amount and maturity date. A Flexi FD places more emphasis on automation and access.

However, early withdrawals may reduce the final return. For example, HDFC Bank states that eligible premature withdrawals, including sweep-in or partial withdrawal, may receive a rate 1 percentage point below the applicable completed-period rate. If the FD remains for less than seven days, the transferred amount earns no interest.5

Therefore, choose an auto sweep FD when withdrawal timing is uncertain and automation matters. A regular FD fits better when the investment amount and maturity date are already clear.

Beyond Parking Idle Cash

A Flexi FD can manage near-term cash, but longer goals require a separate decision about tenure, income and credit risk.

First, retain an emergency buffer. Bank savings and fixed deposits receive DICGC cover of up to INR 5 lakh per depositor per bank, including principal and accrued interest. Eligible balances held in the same capacity are aggregated for this limit.7

Once short-term needs are covered, investors can evaluate other fixed-income options based on their goals, holding period and risk appetite.

Those seeking predictable returns for a defined period may consider regular bank FDs. Investors willing to take higher issuer risk for potentially higher interest rates can explore corporate FDs. Corporate bonds may suit those looking for scheduled interest payments, a stated maturity date and a wider choice of issuers and tenures.

Grip Invest provides access to selected corporate FDs and exchange-listed corporate bonds with disclosed interest rates, yields, ratings and investment tenures.

Investors can compare these available opportunities and choose options that align with their income needs, investment horizon and risk profile. Sign up today!

FAQs On Flexi FD Explained

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001