Corporate FD vs Bank FD: Differences, Returns, Risks And Which Is Better?

Fixed deposits are one of the most popular ways to invest in India. It is the first option that comes to mind for a stable, fixed-income investment. However, not all FDs are the same. They are divided into two categories: Bank FD and Corporate FD. Both of them allow investors to invest money for a fixed tenure and earn fixed returns.

Bank FDs are fixed deposits offered by banks, whereas corporate FDs are offered by companies and NBFCs. They differ in terms of return, stability, safety and risk factors. Understanding the Corporate FD vs Bank FD comparisons can help you choose the best option based on your financial goals.

Returns, Risk, And Liquidity Compared

Both corporate fixed deposit and Bank fixed deposit provide fixed returns. However, they differ significantly in terms of safety, liquidity and investor protection.

Here is an easy comparison table to help you understand the difference.

| Features | Bank FD | Corporate FD |

| Return | Around 5% to 8% annually | Around 7% to 9.5% annually |

| Safety | High due to bank regulations | Depends on the company's financial strength and credit rating |

| Deposit insurance | Covered up to ?5 lakh per depositor | No depositor insurance |

| Liquidity | Premature withdrawal allowed with penalty | Premature withdrawal rules differ by issuer and may be more restrictive |

| Credit risk | Very low for reputed banks | Moderate to high, depending on the issuer |

| Taxation | Interest taxable as per the investor's income tax slab | Interest taxable as per the investor's income tax slab |

| Best for | Conservative investors | Investors willing to take higher risk for better returns |

How To Evaluate A Corporate FD Before Investing

Unlike bank fixed deposits, the safety of a corporate FD depends on the financial strength of the issuing company. Before investing, compare the following factors instead of choosing solely based on the advertised interest rate.

| Factor | Why It Matters |

| Credit rating | Higher credit ratings generally indicate stronger repayment capability, although they do not eliminate risk. |

| Financial performance | Consistent profitability, manageable debt levels, and stable cash flows may indicate stronger financial health. |

| Company reputation | Established issuers with a track record of timely repayments may provide greater confidence. |

| FD tenure | Select a tenure that aligns with your financial goals and liquidity requirements. |

| Interest payout option | Choose cumulative or non-cumulative based on whether you prefer wealth accumulation or regular income. |

Factors To Consider Before Choosing Corporate Or Bank FD

Some factors to be considered before choosing corporate FD vs bank FD.

1. Investment Objective

Choose a bank FD if you want to preserve capital and earn predictable returns. However, if your goal is to earn higher returns, then a corporate FD is best for you.

2. Risk Appetite

Bank FDs are suitable for conservative investors because it operates under strict RBI regulations. Whereas corporate FDs carry credit risk because repayment depends on the company’s financial health.

3. Investment Horizon

The investment period also matters. For short-term goals, such as emergency funds or planned expense banks FDs generally provide better flexibility. For long- or medium-term goals, investors can consider corporate FDs if they are comfortable with locking their money for the chosen tenure.

4. Tax Bracket

Interest earned from both bank fixed deposits and corporate fixed deposits is taxable according to the investor’s applicable income tax slab. If you’re in a higher tax bracket, compare post-tax returns instead of looking at advertised interest rates. The effective return after tax may differ significantly.

5. Diversification

Avoid investing your entire fixed income allocation in one place. Diversifying across bank FDs, corporate FDs and other fixed income options can help you gain better returns and reduce risks.

Taxation Of Bank FD And Corporate FD

The interest earned from both bank fixed deposits and corporate fixed deposits is generally taxable according to the investor's applicable income tax provisions.

While both investments may offer fixed interest rates, investors should compare post-tax returns rather than relying solely on advertised returns, especially if they fall within higher income tax brackets.

When comparing two deposits with different interest rates, evaluating the post-tax return can provide a more realistic picture of the income likely to be retained after taxes.

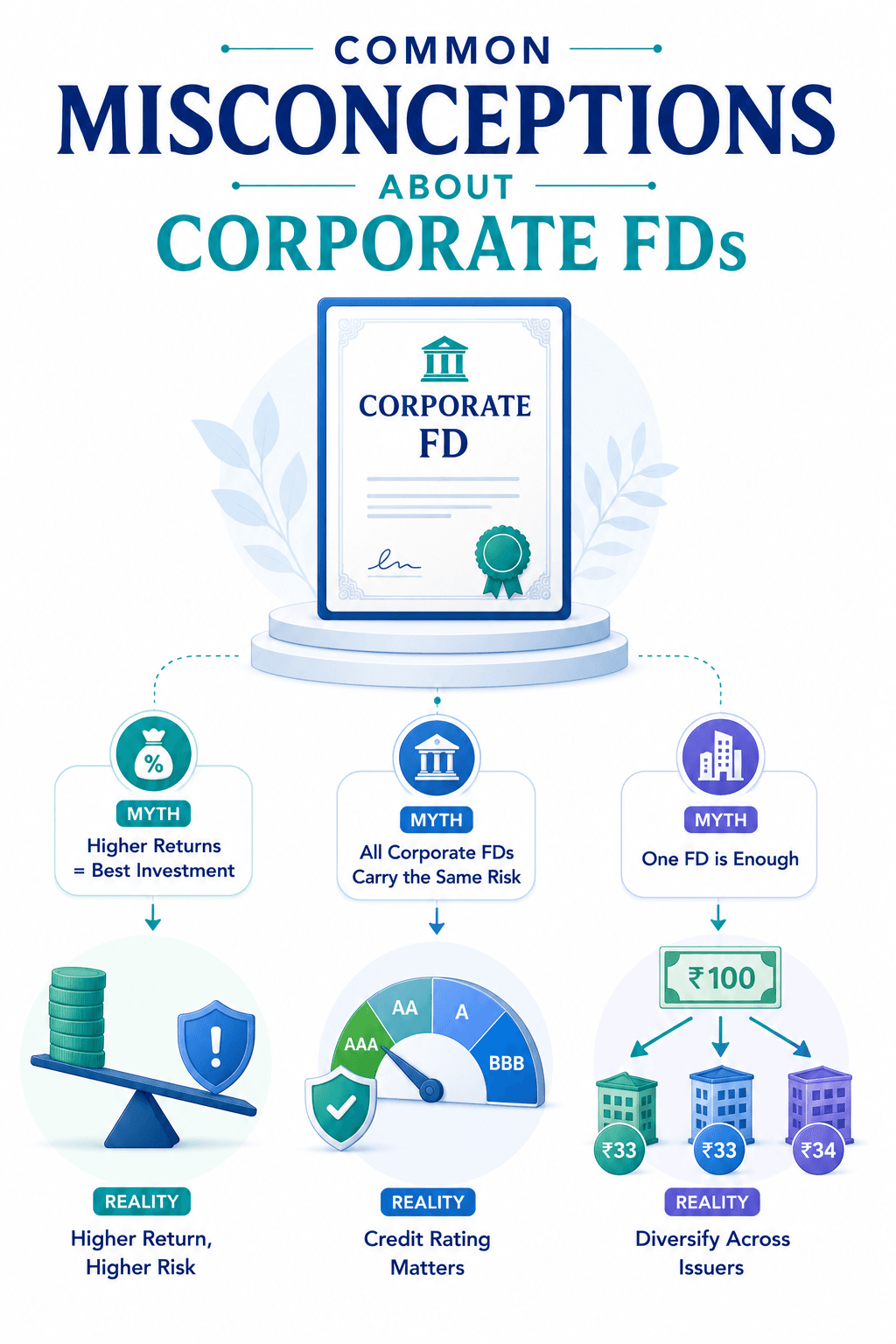

Common Misconceptions About Corporate FDs

Many investors can misunderstand how corporate fixed deposits work. Here are some common misconceptions about corporate FDs.

1. Higher Returns Don’t Always Mean Better Investment

A higher interest rate does not make the investment better. Corporate FDs offer higher returns because they take additional credit risk. Before investing, always assess whether the additional return adequately compensates for the higher risk.

2. Credit Rating Matters

Not all corporate FDs carry the same risk. The credit rating usually depends on agencies such as CRISIL, ICRA and CARE. These agencies reevaluate the issuer's ability to repay investors. Higher-rated corporate FDs indicate stronger repayment capacity.

3. Diversification Reduces Concentration Risk

Putting all your investment into one company can expose you to unnecessary risk. Instead, spreading your investment across different issuers can reduce the impact if one investment underperforms and reduce risk.

Decision Framework: Which FD Fits Different Investor Profiles?

| Investors Profile | Suitable Option |

| First-Time Investors | Bank FDs |

| Retiree seeking stable income | Mostly Bank FDs with limited exposure to highly rated Corporate FDs |

| Moderate-risk Investors | Combination of Bank FDs and Corporate FDs |

| Investors seeking higher fixed returns | High-rated corporate FDs |

| Short-term emergency fund | Bank FD |

When Does A Bank FD Make More Sense?

A bank fixed deposit may be a more suitable choice when:

- Capital preservation is the highest priority.

- Funds may be required before maturity.

- The investment forms part of an emergency fund.

- The investor has a low tolerance for credit risk.

- Simplicity and regulatory protection are more important than earning higher returns.

In such situations, the lower risk profile of bank FDs may outweigh the potential for higher returns offered by corporate FDs.

When Can A Corporate FD Be Considered?

A corporate FD may be suitable for investors who:

- Are comfortable taking a measured level of credit risk.

- Seek potentially higher fixed returns.

- Have already built an emergency fund elsewhere.

- Are willing to compare issuers based on their credit quality rather than only on interest rates.

- Intend to diversify across different fixed-income investments instead of relying on a single issuer.

Choosing a corporate FD should involve evaluating both the issuer's financial strength and the investor's own risk tolerance.

What Happens If A Corporate FD Issuer Faces Financial Difficulty?

Unlike bank fixed deposits, corporate FDs are not covered by deposit insurance. If the issuing company experiences financial stress, interest or principal repayments may be delayed or, in some cases, defaulted.

Although investing in higher-rated corporate FDs may reduce credit risk, no fixed-income investment is entirely risk-free. Investors should therefore review the issuer's latest credit rating, financial performance, and other disclosures before investing. Diversifying investments across multiple issuers instead of concentrating money in a single corporate FD can also help manage risk.

Building A Diversified Fixed Income Portfolio

Both bank FD and corporate FD are great investment options. Therefore, it is not important to choose between the two. You can choose both for a diversified portfolio. It will combine multiple investment options based on your financial goals, investment horizon and risk tolerance.

Investors can keep their emergency funds in bank FDs for maximum safety while allocating a portion o their long-term investment in highly rated corporate FDs for potentially higher returns. Investors can also consider corporate bonds that offer another source of fixed income. Platforms like Grip Invest provide access to fixed-income opportunities like corporate bonds that help investors diversify beyond traditional deposits.

Conclusion

The choice between Corporate FD vs Bank FD depends on your financial priorities. You can choose a bank FD for capital safety because of its regulatory oversight and deposit insurance. However, if you are comfortable taking credit risk for potentially higher returns, then you can select a highly rated corporate FD after evaluation.

Investors can choose both rather than choosing only one investment option. Diversification across bank FDs, corporate FDs and other investment options is also necessary for building wealth. Explore more fixed-income investment opportunities with Grip Invest. It is a platform built for investors looking for diversfiying their portfolio that balances stability, returns and long-term financial growth.

FAQs On Corporate FD Vs Bank FD

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001