How To Calculate FD Interest: Formula, Examples, And Tips

The Indian investment landscape comprises a range of assets, from high-risk growth instruments to low-risk, fixed-income securities. However, one asset has remained a popular choice among investors, despite the growing modernisation and dynamic changes in the segment. This asset category is fixed deposits.

Despite its popularity and consistent use, many users overlook the nuances of calculating FD interest, resulting in lower returns.

Contrary to popular belief, the FD maturity amount calculation has various aspects that determine the returns.

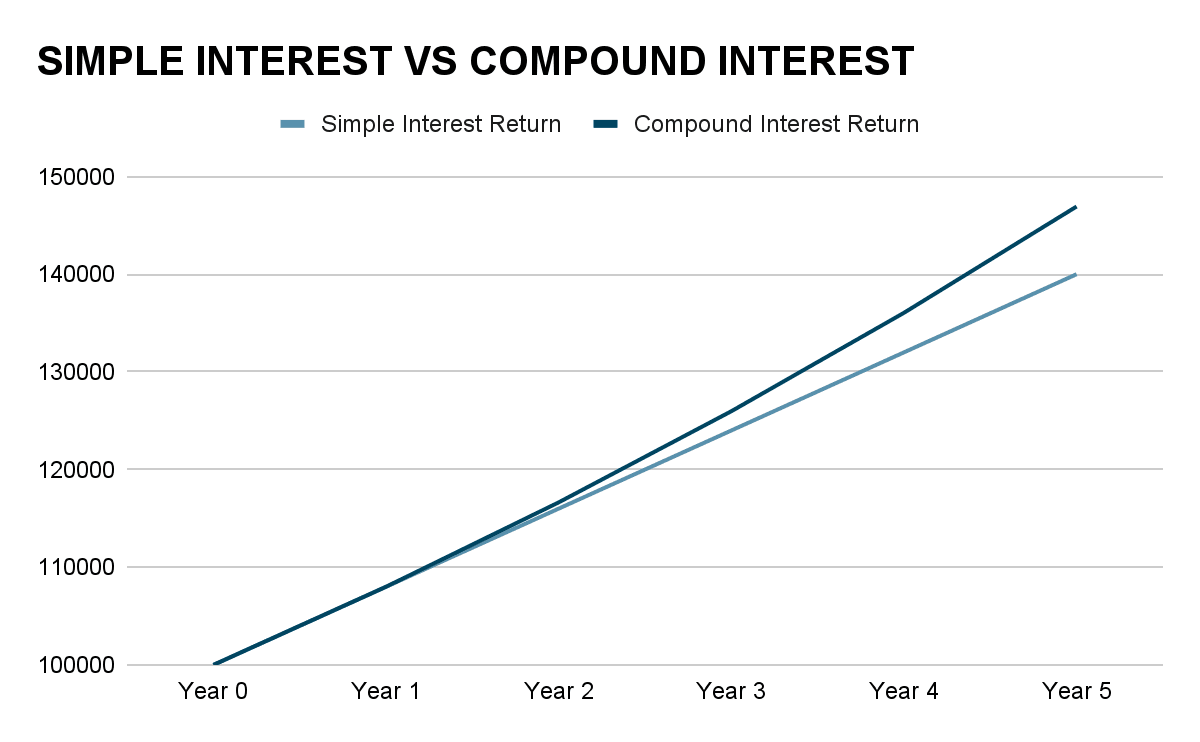

A key aspect is whether the return rate is simple interest or compound interest. If simply the mathematical difference is considered, assuming an investment of INR 1 lakh for 5 years, the graph shows the impact of 8% simple interest vs 8% compounds interest.

The fact that compound interest returns beat the simple interest yield over the long-term might be well-known, but investors often think that a fixed deposit fundamentally compounds interest. If you think so too, this detailed guide on how to calculate FD interest is a must-read.

Types Of FD Interest Calculation

There are two ways to calculate the FD interest rate. These two types of FD interest are simple interest and compound interest. Let us analyse how each of these mechanisms operates, their FD interest formula, and more, to optimally understand how to calculate FD interest.

1. Simple Interest FD

Under the simple interest FD formula, interest is calculated only on the principal amount for the entire tenure. In this case, interest earned is not reinvested; it is accumulated or paid linearly. Simple interest is levied on FDs in the case of short-term deposits or non-cumulative deposits.

In the case of non-cumulative deposits, since the interest earned is paid out to the customer monthly or quarterly, the return does not get accumulated, resulting in a simple interest rate.

For instance, if Mr K invests INR 10,000 in a non-cumulative FD that pays 8% p.a. return. In the first year, 8% return is calculated on INR 10,000. In the second year as well, since the interest of the first year is paid out to the investor, interest is levied on INR 10,000 only.

A similar situation occurs for short-term deposits, or deposits of one year or less. Such FDs do not have enough time to benefit from the impact of compounding, as most FDs are usually compounded annually. The priority of these short-term FDs is to maintain liquidity and security, whilst optimising fund usage.

2. Compound Interest FD

Primarily, a majority of deposits earn compound interest, provided that they are cumulative and have a sufficient tenure (usually over a year). In the case of compound interest, the interest rate is levied not only on the principal, but also on the interest accrued. Therefore, this interest-on-interest effect is the primary feature that distinguishes compound interest from simple interest.

The main goal of a compound interest fixed deposit is to offer stable growth through fixed returns.

This enhances portfolio stability and investor confidence during volatility or high-risk investments.

Since the distinction between simple and compound interest stems from their meaning, to effectively understand the difference between the two, an investor should analyse the FD interest formulas.

FD Interest Formula Explained

The formula for simple interest is simple and self-explanatory. The simple interest FD formula is given below.

Simple Interest (SI) = (P × R × T) / 100

Where, P = Principal or the original amount invested

R = Rate of interest

T = Time or tenure for which the deposit is made

For instance, if Mr K invested INR 10,000 at 6% p.a. interest for 2 years, the interest earned by him at the end of this tenure would be INR 1,200. Therefore, his total amount becomes INR 11,200. However, when it comes to compound interest, there are a few more aspects.

Discussed below is the compound interest formula used to calculate the total amount after compounding interest is levied.

A = P × (1 + r/n)^(n×t)

Where A = Total amount after a particular tenure

P = Principal

r = Rate of interest

n = Compounding frequency

t = Tenure

When the principal is deducted from this amount, we get the value of total interest earned.

Therefore, Compound Interest (CI) = A - P

Where A = Amount calculated with the first formula

P = Principal

While parameters like the principal, return, and tenure are common across both simple interest and compound interest, the variable n or compounding frequency requires a nuanced look.

Compounding Frequency

The number of times interest is calculated and added to the principal in a particular year is called compounding frequency. For example, in a quarterly compounding FD formula, the value of n will be 4 because quarterly interest compounding means interest is levied 4 times in a year. Similarly, if interest is compounded half-yearly, then the interest is calculated twice a year, meaning the value of n will be 2.

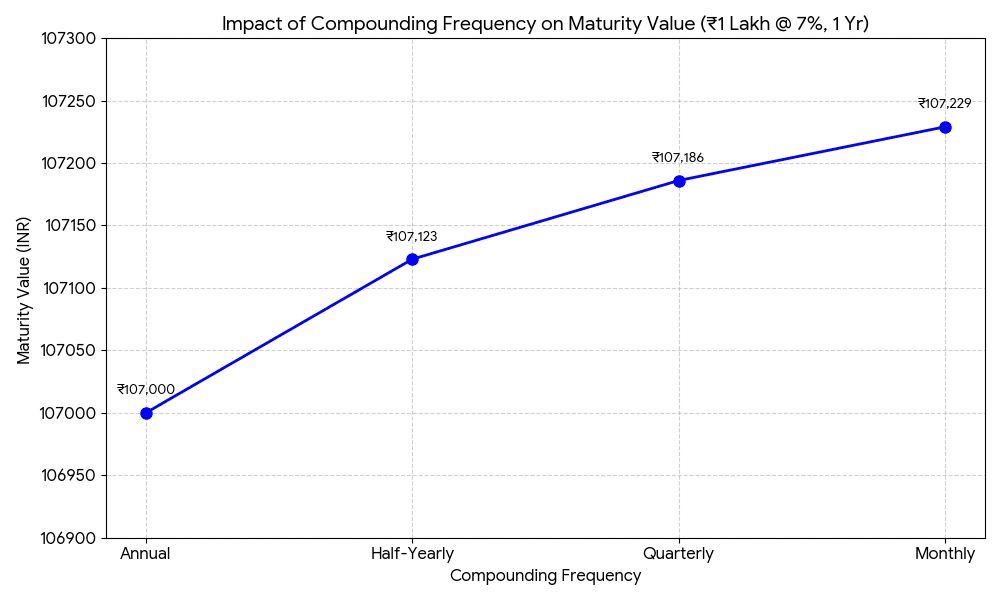

The graph below is an FD interest calculation example to show the impact of compounding frequency on returns, assuming an INR 1 lakh FD, with 7% p.a. interest for 1 year.

The graph clearly illustrates how, even on a 1-year horizon, a quarterly, half-yearly, or monthly compounding adds additional returns. Although the per annum interest remains the same at 7%, when interest is compounded more than once, given the interest-on-interest concept of compound interest, the accrued value on which interest is levied expands. Thus, the total return also increases.

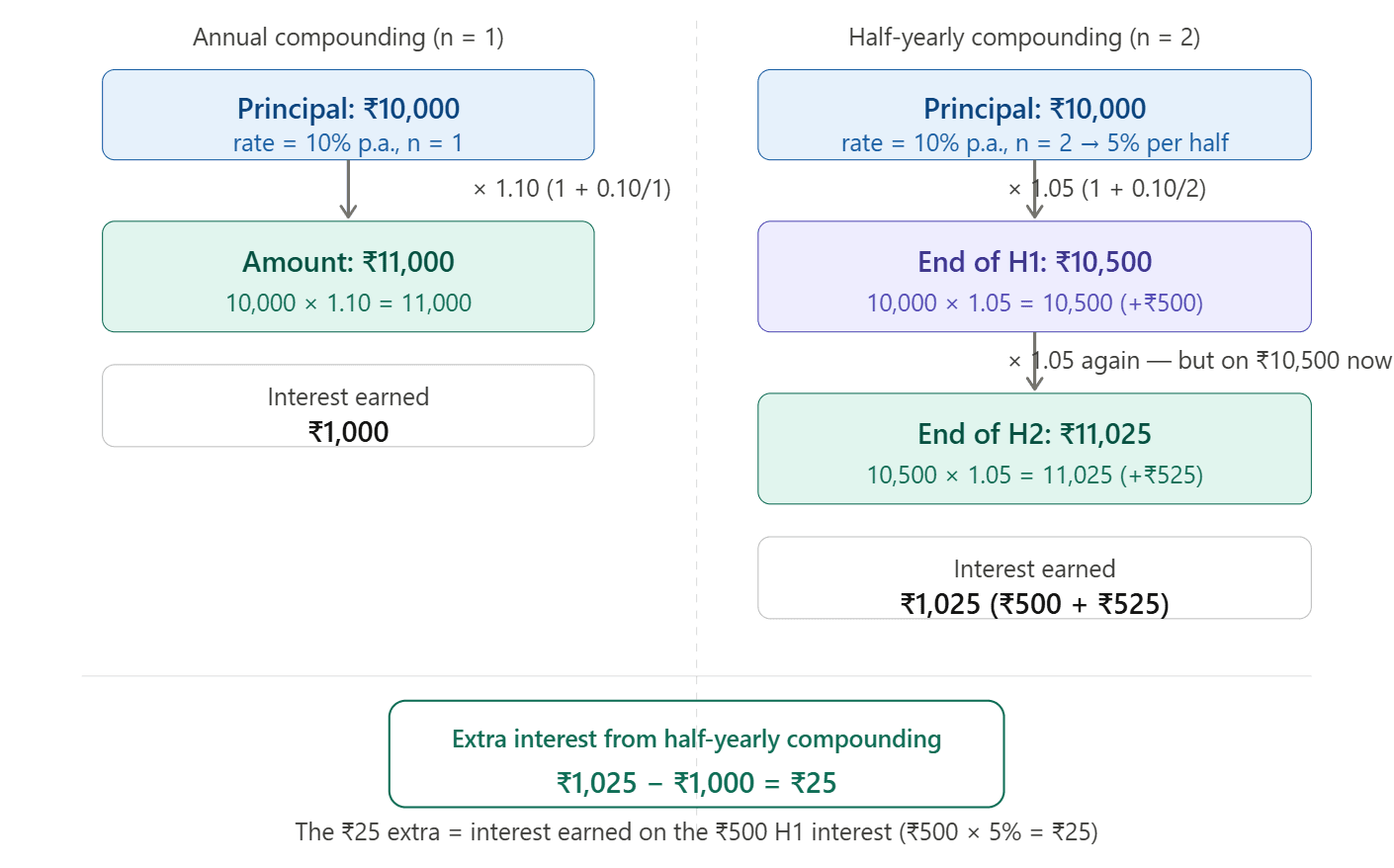

For example, INR 10,000 is invested for 1 year at 10% p.a. If interest is compounded annually, he will earn an interest of INR 1000, as the total amount becomes INR 11,000. If the interest is compounded half-yearly, the effective interest for each half-yearly period is 5% (10/2). In the first half, the principal is INR 10,000, and at 5% interest, the amount becomes INR 10,500. Now, interest is calculated on INR 10,500 (the base expands). At 5% interest, the final amount is INR 11,025. Thus, through half-year compounding, the return increased.

Now, let us take an example to understand how compounding helps wealth to grow over the long-term.

Examples Of FD Interest Calculation

The amount of interest varies with different circumstances. Let us take examples to understand some key return trends.

- Cumulative VS Non-Cumulative FD Returns

Suppose Mr K and Mr M invest INR 10,00,000 each for a period of 10 years at 7% interest. However, while Mr K’s FD is cumulative, meaning the interest matures with the principal after tenure ends, Mr M withdraws the interest monthly.

After 10 years, Mr K earns an interest of INR 9,67,151, resulting in the total amount becoming INR 19,67,151. However, since Mr M withdrew the interest, rather than reinvesting it, the interest gets calculated at simple interest. Therefore, he withdrew a total of INR 7,00,000 (total interest) and the principal of INR 10,00,000 is repaid on maturity.

Notice how Mr K earned about INR 2.67 lakhs more than Mr M. This is because Mr M did not earn interest on interest.

- Impact of Tenure

Suppose both Mr K and Mr M invested INR 1,00,000 at 7%. While both FDs are cumulative, Mr K invests for 1 year, while Mr M invests for 5 years. On maturity, Mr K would earn INR 7,000 interest, while Mr M would earn INR 40,255 as interest.

Undertaking such calculations online is tedious and error-prone. Therefore, the FD calculators in India help automate calculations and enable investors to calculate anticipated returns before undertaking an investment. FD calculators of SBI, HDFC, ICICI, or Grip enable FD return calculations in a fraction of a second.

This understanding of how to calculate the monthly FD interest payout and other return forms can aid in optimal FD investment. However, traditional fixed deposits are not the only fixed-income investments.

FD Vs Other Fixed Income Investments

Fixed deposits are a reliable savings tool, but their returns often struggle to outpace inflation, especially when the Consumer Price Index (CPI) hovers around 4% to 5% annually.

With most bank FDs offering 6.5% to 7% pre-tax returns, the real post-tax yield for investors in the 30% tax bracket can drop to as low as 4.5% to 5%, barely keeping pace with inflation.

This is where alternative fixed income instruments offer a meaningful advantage. Here is how KVB FDs compare against other popular fixed income options:

| Investment | Returns | Safety | Liquidity | Tax Benefit |

| KVB FD | 6.25% to 6.80% | High (DICGC insured up to ?5 lakh) | Moderate (premature withdrawal with penalty) | 80C for tax saver FD |

| Corporate FDs (Grip) | 8% to 10% | Moderate (NBFC-issued, uninsured) | Low to moderate | No |

| Corporate Bonds (Grip) | 9% to 12.5% YTM | Moderate to high (rated instruments) | Moderate (secondary market) | No |

| Government Securities | 7% to 7.5% | Highest (sovereign guarantee) | High (exchange traded) | No |

| Debt Mutual Funds | 6% to 8% | Moderate | High (T+1 redemption) | Indexation benefit |

Conclusion

Understanding how to calculate FD interest is essential for making informed investment decisions and maximising your returns. Whether your deposit earns simple interest or compound interest, factors like tenure, compounding frequency, and payout structure can significantly impact your final maturity amount.

While fixed deposits remain a reliable option for stable and predictable income, investors today must look beyond just safety. Evaluating returns in the context of inflation and comparing different fixed income options can help build a more efficient and balanced portfolio.

By using the right FD interest formula or online calculators, you can plan your investments better, choose the right tenure, and align your returns with your financial goals.

If you are looking to go beyond traditional FDs and explore higher-yield fixed income opportunities, platforms like Grip Invest can help you discover curated investment options with better return potential and transparency.

FAQs

1. How is FD interest calculated?

In the case of simple interest, FD interest is levied on the principal alone. However, in the case of compound interest, FD interest is levied on the principal and the total interest accrued.

2. What is compound interest in FD?

In the case of compound interest, the interest rate is levied not only on the principal, but also on the interest accrued. Therefore, this interest-on-interest effect enables exponential capital growth.

3. Which FD gives the highest returns?

High-yield FDs, also known as corporate FDs, can offer higher interest than regular FDs. On Grip, investment-grade high-yield FDs offer 8-10% returns, with both cumulative and non-cumulative payment options.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001