Junk Bonds Explained: High Returns Or High Risk For Indian Investors?

Junk bonds or high-yield bonds are corporate bonds rated below investment grade, so issuers offer higher coupons to compensate for weaker credit profiles. For Indian investors, these instruments can look attractive when bank deposits or high-quality debt feel limiting, especially in a low real-return environment.

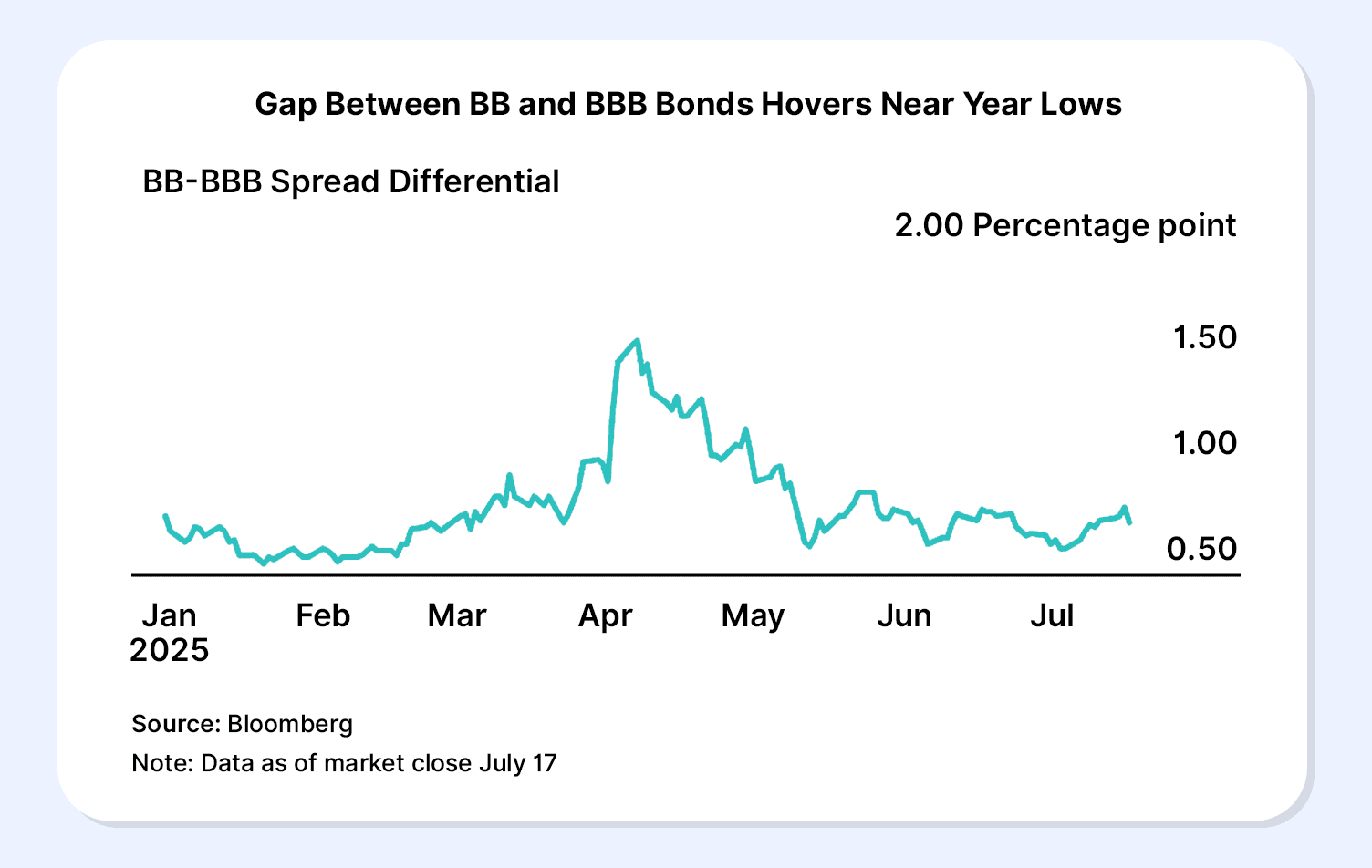

Globally, the search for yield has already pushed risk premiums lower. In the US, for example, the gap between top-tier high-yield and lower-rated investment-grade bonds is now under one percentage point1. Such tight spreads show how easily markets can underestimate credit risk. That extra yield is never free.

Source: NDTV profit2

Lower-rated issuers face a higher chance of default, and prices can swing sharply when growth slows or sentiment turns. Many retail investors in India focus on the headline return and underestimate how quickly losses can add up.

This article explains junk bonds’ meaning, how they work, highlights key risks, and helps you judge if they fit your portfolio.

What Are Junk Bonds?

Around 11% of FY24 Indian corporate bond issuance carries a rating below BBB on the credit scale3. This segment sits in the high-yield or junk bond universe, where investors accept more risk for the chance of higher income.

Here, issuers pay more to borrow. They usually have weaker balance sheets, higher debt levels, or more uncertain business prospects than investment-grade names. To compensate for this extra credit risk, issuers offer higher coupons, and investors accept greater price volatility and default risk in return. Understanding where ratings sit on the scale helps you see why these instruments can look tempting yet carry a meaningful downside.

Credit rating | Risk view |

AAA | Very low credit risk |

AA | Low credit risk |

A | Adequate protection |

BBB | Moderate risk, more sensitive to stress |

BB | Clear default risk |

B | High default risk |

CCC or C | Very high risk, near distress |

D | In default |

Why Investors Are Attracted To Junk Bonds

As noted earlier, higher coupons and double-digit yields can quickly draw attention in a low-return environment. For many retail investors, such offers seem like a faster way to reach income goals than other options in the debt market.

Key reasons often draw investors towards this segment

- Higher income potential: Some lower-rated issues in India offer yields around 12 to 14%, compared with roughly 6 to 7% on safer instruments, which makes the gap hard to ignore4.

- Scope for capital gains: If the issuer’s finances improve and the credit rating moves up, market prices can rise, adding price gains to the regular coupon income.

- Diversification appeal: Returns may move differently from government securities or blue chip equity, so some investors use a small allocation to seek a different return pattern.

- Priority over shareholders: In a stress or default situation, bondholders stand ahead of equity holders in the payout queue, which can offer some recovery cushion.

Key Risks Of Junk Bonds

Junk bond returns may look like easy income. The same features that attract investors also increase the chance of permanent loss when conditions turn.

Here are the junk bond risks:

1. Credit and default risk: Issuers already have weaker finances, so any stress in cash flows or funding can lead to missed interest or principal, in extreme cases, a loss of most of the invested amount.

2. Downgrade and price swings: If a rating agency cuts the grade further, market prices can fall sharply, and exiting in time becomes difficult.

3. Liquidity risk: Trading volumes are often thin, so investors may struggle to sell at a fair value during periods of market stress.

4. Interest rate and macro risk: When safer yields move up or the economy slows, risk appetite can collapse, leaving holders stuck with lower prices and limited buyers.

Historical Default Rates Of Junk Bonds

There is no single official long-run series that shows a “junk bond default rate” for India. Instead, rating agencies publish detailed default histories for sub-investment-grade categories such as BB, B, and C.

Here are CRISIL’s long-run cumulative default rates (CDRs) (FY2015-FY2025)5

Rating category | One-year | Two-year | Three-year |

CRISIL BBB | 0.46% | 1.27% | 2.21% |

CRISIL BB | 2.86% | 6.19% | 9.92% |

CRISIL B | 8.40% | 17.21% | 25.76% |

CRISIL C | 24.98% | 40.94% | 52.83% |

This table makes the risk gradient clear. Then CDRs climb steeply in BB, B and C.

India Ratings and Research provides a second lens through its FY2025 transition and default study, which shows that BB and below issuers default far more often than investment-grade names6.

Over the ten-year window (FY2016-FY2025), the overall annual default rate across its rated universe averages around 2%, which already tells you that outright failure is not the norm for rated issuers. Within that average, however, risk is very unevenly distributed.

- Sub-investment-grade issuers (BB and below) default far more often. Their annual default rate generally sits in the 2-9% band, with a spike to about 8.5% in FY2020 during the COVID-related stress, before easing to about 2.3% in FY2025.

- Investment-grade names (BBB and above) show much lower realised risk, with annual default rates mostly near or below 1.5%

Here are the 10-year adjusted CDRs:

Rating bucket (long-term) | 1-year (%) | 2-year (%) | 3-year (%) |

IND BB | 4.5 | 8.3 | 11.3 |

IND B | 5.9 | 10.7 | 15.2 |

IND C | 36.5 | 42 | 44.8 |

Sub-investment grade | 5.1 | 9.2 | 12.7 |

Investment grade | 0.7 | 1.8 | 2.9 |

- Over a 3-year holding period, historical data suggests that about 12-13% of below investment-grade bonds have defaulted, compared with under 3% of investment-grade names.

- Within the junk bucket, risk climbs as you move down the ladder. Three-year CDRs rise from around 11.3% at BB-rated bonds to 15.2% at B, and reach an extremely high 44.8% for C-rated entities.

- The data, therefore, indicates that junk bonds do not all fail at once, but the probability of loss is several times higher than in investment-grade paper, especially once you go below BB.

Junk Bonds Vs Investment-Grade Bonds

These default patterns highlighted the risk-return continuum. Investment-grade bonds sit at the lower-risk end. Their issuers usually have stronger finances, more predictable cash flows, and lower default probabilities, so yields are lower. At the other end, junk bonds in India offer higher coupons but expose investors to a much greater default risk.

Within investment grade, A and AA-rated corporate bonds often act as a middle ground. They usually offer higher yields than AAA bonds issued by top corporates, public sector entities, or sovereign-linked borrowers, yet still sit above the junk threshold.

Securitised debt instruments (SDIs), such as asset-backed or receivables-backed structures, add another layer to this spectrum. Well-structured SDIs, backed by diversified pools of loans or leases and supported by credit enhancements, may carry A or AA ratings while offering yields above many plain-vanilla corporate bonds.

Regulated platforms that curate A and AA-rated bonds and SDIs aim to filter this universe further. They typically shortlist issuances based on rating, security, cash-flow visibility, and issuer track record, so investors can look for enhanced yields without going all the way down the junk spectrum.

Conclusion

Junk bonds in India can deliver higher returns, but those gains come with significantly higher credit and default risk. As rating data shows, the probability of loss rises steeply once you move below investment grade, making careful due diligence essential. For most investors, junk bonds should never be the core of a portfolio and must only be considered if risk appetite, liquidity needs, and goals allow it. Safer alternatives like A and AA-rated corporate bonds or well-structured SDIs offer a better balance of yield and stability. A diversified, long-term approach usually works better than chasing high coupons in isolation.

To explore curated, high-quality bonds and structured debt opportunities, visit Grip Invest and start building a smarter debt portfolio.

FAQs On Junk Bonds

1. What exactly makes a bond “junk”?

Typically, it is a security rated below investment grade, such as BB or lower on credit rating scales. Such instruments carry higher credit risk and usually offer higher yields to compensate.

2. Are junk bonds available in India?

Yes, high-yield, sub-investment-grade corporate bonds do exist in the domestic market. They are usually accessed through specific issuances, debt mutual funds, or curated bond platforms rather than broad public offerings.

3. Why do junk bonds offer higher returns?

Investors typically receive a higher coupon on these securities to compensate for the greater chance of delayed payments or default. The extra yield reflects weaker credit profiles and more uncertainty around future cash flows.

References:

1. Live mint, accessed from: https://www.livemint.com/market/bonds/aaa-to-junk-what-are-credit-ratings-and-why-every-bond-investor-must-check-this-before-investing-explained-11763552567183.html

2. NDTV profit, accessed from: https://www.ndtvprofit.com/markets/junk-bond-investors-pile-into-the-riskiest-debt-credit-weekly

3. Financial express, accessed from: https://www.financialexpress.com/business/economy-explained/the-truth-behind-the-12-14-returns-in-bonds/3990581/

4. CRISIL, accessed from: https://www.crisilratings.com/content/dam/crisil/our-analysis/publications/default-study/crisil-ratings-annual-default-and-ratings-transition-study-fy-2025.pdf

5. India ratings, accessed from: https://www.indiaratings.co.in/data/Uploads/TransitionandDefaultStudy.pdf

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001