Neobanks In India: Are They The Future Of Digital Banking?

Over the past decade, banking in India has moved from queues at branches to taps on a screen. Around 87% of online Indian adults say they want to manage all their banking through a smartphone (in 2023)1.

This shift sits on top of a powerful digital backbone. India accounts for about 46% of global real?time digital payment transactions (largely driven by UPI)2. Retail digital payments have risen almost 90x in 12 years between FY2012–13 and FY2023–24, and policymakers continue to push UPI, Aadhaar, and account aggregation.

In this environment, app-first players have flourished, taking neobank users from 6 million in 2021 to a projected 60 million by 2027, with more than 20 platforms in the market3.

Yet an app-only interface is just the entry ticket. The real story is how neobanks in India reimagine product design, pricing, data use, and partnerships with licensed banks behind the scenes.

What Are Neobanks?

Neobanks are entirely digital entities offering financial services through mobile applications and web interfaces. They deliver familiar functions such as savings, payments, cards and financial tools, but without any physical branch presence. Their operations depend on technology, intuitive design, and data-driven insights rather than traditional infrastructure.

India currently has no true full-stack digital banks. Meaning there is no digital-only bank that has its own RBI banking licence, its own balance sheet, and can take deposits and lend directly, similar to Starling or Monzo in the UK.

This is because the RBI has not created a separate ‘digital bank’ licence so far. NITI Aayog has proposed a framework for full-stack digital banks, but this remains a proposal, not a live licence category4.

Therefore, the current neobanks in India sit on top of partner banks and/or hold NBFC licences, so they cannot independently accept deposits as a bank.

Also Read: RBI Banking Reforms 2025: Key Updates For Investors, Banks And Corporates

Key types you will see in the Indian market include:

1. Digital banking units of traditional banks

These are app-first arms of existing banks. For example, SBI YONO or Kotak811 use the parent bank’s licence and balance sheet but offer a distinct digital experience.

2. Front-end neobanks

These sit on top of partner banks. Fi Money and Jupiter work with Federal Bank and others for accounts and cards5,6.

3. SME and cash-flow focused platforms

Some neobanks specialise in business banking. RazorpayX, for instance, offers current accounts and payouts in partnership with banks such as RBL Bank and ICICI Bank7.

Why Neobanks Are Growing In India

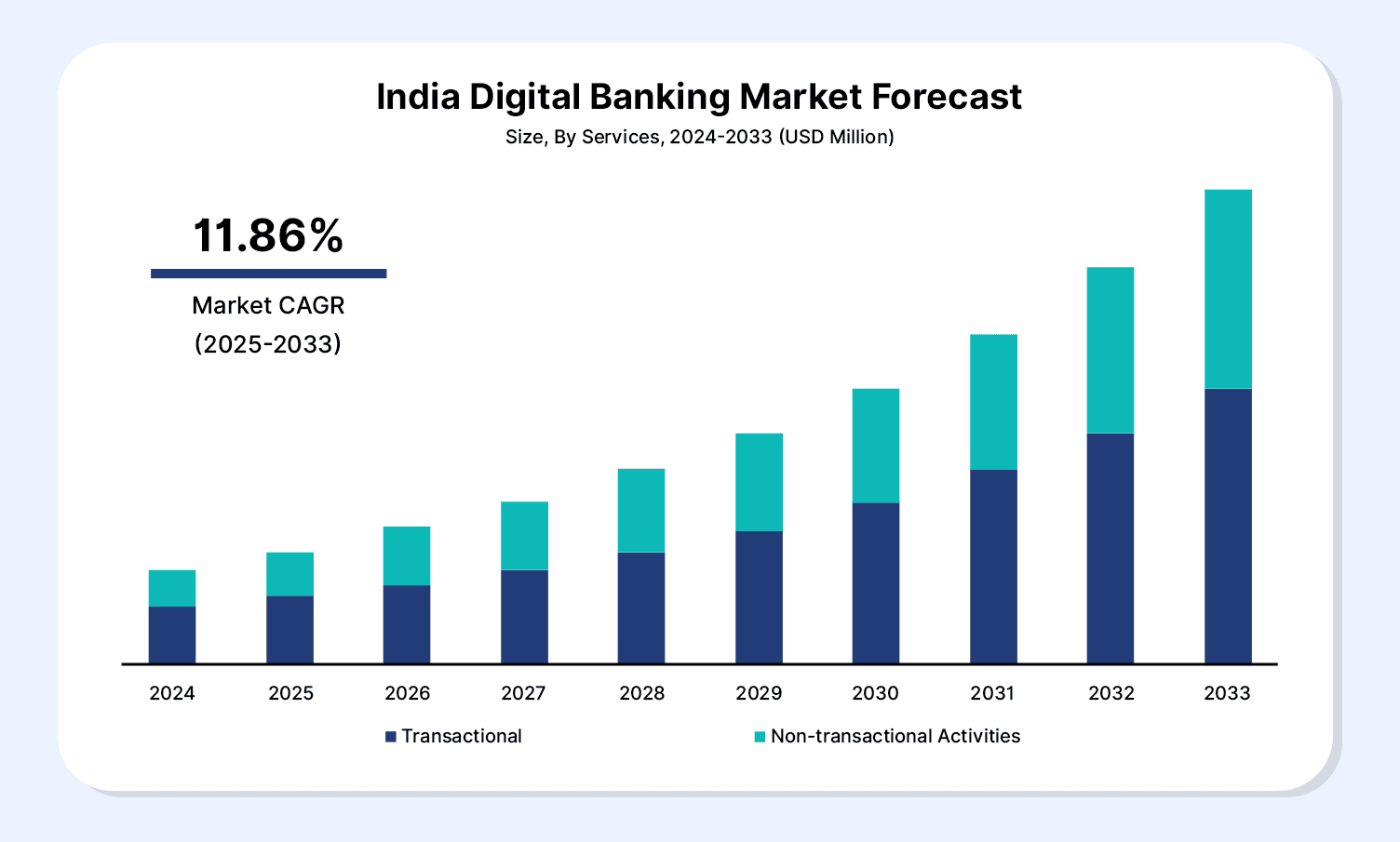

Digital banking (India) market size/revenue has scaled sharply. The market, valued at about USD 341.5 million in 2024 and is expected to climb to USD 936.2 million by 2033, reflecting an annual growth rate of 11.86%.

Source8

This steady rise underlines a wider shift in how people and businesses engage with money. Here are some of the reasons why neobanks can be the next big thing in India.

1. Millennial and Gen Z user behaviour

Younger users lead this shift, and a 2025 study reports that about 67% of Gen Z and Millennials use neo banking platforms9. These users prefer convenience, personalisation and real-time control instead of traditional brand loyalty.

2. Faster onboarding and UX

Digital KYC and video journeys let providers open accounts within minutes, so platforms can offer smooth, paperless onboarding compared with slower branch-led processes.

3. MSME-focused product innovation

India’s MSME sector, with a credit gap estimated at INR 20–25 trillion, is fuelling demand for smarter, integrated tools10. Neobanks serve this market through platforms that blend current accounts, payments, invoicing, and cash-flow-based credit access.

Also Read: Why Global Banks Are Pouring Into India: And What It Means For Investors

Key Features Of Neobanks

These platforms put everyday banking on smartphones and browsers. For neobanks, the priority is swift access, uncluttered design and the ability to act quickly without queues or paperwork.

1. Digital onboarding and account management: Customers open accounts, complete KYC and manage cards within minutes in the app, with clear prompts that keep the whole journey straightforward.

2. Continuous visibility of money movements: Balances and transactions refresh almost instantly, while timely alerts for successful, declined, or unusual activity create a live view of cash flows.

3. Transparent pricing with embedded tools: Service charges and foreign exchange markups appear clearly before confirmation, and built-in budgeting tools organise spending into categories and simple saving goals.

4. Security with fine-grained controls: Encryption, multifactor checks and biometric entry protect access, while app controls let users adjust usage settings or freeze a card immediately if needed.

Also Read: Canara Bank FD Interest Rates 2025: Latest Rates, Tenure Options, and Safer Alternatives

Risks And Limitations Of NeoBanks India

App-based banking brings convenience, but it also introduces practical vulnerabilities that customers need to understand before relying on a single app for everything.

Regulation and partner reliance: Many digital providers in India operate on top of licensed banks or NBFCs rather than holding their own licence. If that partner revises its risk appetite or faces stress, limits, pricing, or even onboarding rules can change quickly for end users.

Safeguards for money and service continuity: Balances usually sit with the underlying institution, so deposit protection flows from that entity rather than the consumer brand. Any outage, network disruption, or KYC issue can temporarily restrict access because there is no branch network as a fallback.

Product scope, data use, and sustainability: Offerings tend to centre on payments and simple deposits while collecting detailed behavioural data. Many players are still working towards durable profitability, so shifts in funding or regulation can trigger consolidation or abrupt strategy changes.

Also Read: RBI Repo Rate Cut In 2025: Best Investment Moves To Make Right Now

Why Fixed Income Still Matters For Users Of Neobanks

Neobanks make it easy to spend and save, but they do not replace the need for stability. Fixed-income products help protect capital and bring predictability to a digital-first portfolio.

- They balance risk by offsetting equity or volatile assets with steadier returns.

- They put idle app balances to work, instead of leaving money in low-yield accounts.

- Defined interest and maturity make it easier to plan EMIs, fees and short-term goals.

Grip offers curated, regulated fixed-income options, so users can move surplus from digital accounts into predictable-return instruments without leaving the comfort of an online, app-led experience.

Conclusion

Neobanks in India are transforming the digital banking landscape by offering seamless, app-first financial services tailored to the needs of Millennials, Gen Z, and MSMEs. While they operate through partnerships with licensed banks and face regulatory and operational challenges, their quick onboarding, transparent pricing, and innovative credit solutions position them as key players in the future fintech ecosystem.

As digital banking continues to grow rapidly, neobanks will play a vital role in shaping an inclusive, efficient, and customer-centric financial experience in India. Complement your neobank balances with Grip Invest’s curated fixed-income options for up to 12.5% fixed returns and true portfolio stability.

FAQs On Neobanks In India

1. How do neobanks differ from traditional banks?

Digital-only players prioritise app-based onboarding, lean operations, and partnerships with licensed institutions. Conventional banks usually combine physical branches, broader service menus, and direct balance-sheet banking under one roof.

2. Can you invest through neobanks?

Many of these digital platforms now offer access to mutual funds, fixed deposits, or other products within the app. The specific options you see typically come through tie-ups with regulated brokers, asset managers, or partner banks.

3. Are neobanks regulated?

In India, most digital-first banking apps sit on top of RBI-licensed banks or NBFCs, with legal responsibility resting with the partner institution. Deposit safety comes from the underlying bank’s licence and the broader fintech, KYC and data-protection rules.

References:

1. Forrester, accessed form: https://www.forrester.com/blogs/digital-experience-strategy-for-banks/

2. PWC accessed from: https://www.pwc.in/assets/pdfs/indian-payment_handbook-2024.pdf

3. IBEF, accessed from: https://www.ibef.org/blogs/neobanks-rising-millennial-banking-in-a-digital-first-india

4. PIB, accessed from: https://www.pib.gov.in/PressReleasePage.aspx?PRID=1843259

5. FI money, accessed from: https://fi.money/FAQs/about-fi/general-info/is-fi-money-a-bank

6. Jupiter Money, accessed from: https://jupiter.money/

7. Razorpay, accessed from: https://razorpay.com/x/current-accounts/

8. IMARC, accessed from:https://www.imarcgroup.com/india-digital-banking-market

9. Kadence money, accessed from: https://kadence.com/knowledge/indias-youth-embrace-neo-banks/

10. PIB, accessed from: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2038541

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001