NPS Vatsalya Scheme: Retirement Planning For Children Explained

Successful investing begins with setting a goal, an objective that investors want to achieve through the corpus they have built. While different investors have different goals, one remains constant, which is retirement. Investors invest in their working years to ensure access to periodic returns that can act as passive income or a lump sum corpus during retirement or non-working years. Therefore, the sooner an investor commits to retirement planning and investing, the greater will be their accumulated corpus on retirement. However, according to a report from PGIM India in 2025, despite retirement becoming a leading goal, only 37% of respondents have a plan, down sharply from 67% in 20231. Besides procrastination and trust deficits, lack of knowledge remains a vital obstacle.

Therefore, this blog decodes the NPS Vatsalya Scheme, a long-term investment for kids that allows early retirement planning. Launched in September 2024 by Finance Minister Nirmala Sitharaman, this scheme extends the purview of the National Pension System (NPS) to include children below 18 years of age2. Parents or guardians can utilise this structured, low-cost, long-term investment vehicle to build a corpus for their children. Primarily, this child NPS scheme is not just a savings product, but an effective tool to create generational wealth and financial security. Let us explore the NPS Vatsalya scheme in detail and understand its features, benefits and risks.

What Is The NPS Vatsalya Scheme?

The NPS Vatsalya Scheme, a child-specific version of the National Pension System (NPS) in India, is administered by the Pension Fund Regulatory and Development Authority (PFRDA). Guardians or parents make periodic contributions to the minor pension account until the child reaches 18 years of age. Post 18 years, this child pension plan in India is transformed into a standard NPS account. Furthermore, similar to regular NPS investments, the NPS Vatsalya Scheme contributions are invested in a mix of debt and equity assets.

Key objectives of the scheme are presented below:

- From a young age, investors can cultivate a disposition of long-term investing and financial restraint.

- It provides a structured, regulated, and low-cost retirement savings from a young age.

- Investors can optimise the impact of compounding through early investments.

- NPS Vatsalya addresses the retirement savings deficit by encouraging early participation.

- Investors can build a significant corpus that can be used not only for retirement but also to fulfil other needs like education, illness, and so on.

Overseas Citizenship of India (OCI) Cardholders and Non-Resident Indians (NRIs) are eligible to participate in the child NPS Scheme, besides regular citizens, provided that they have the following documents.

Particulars | Documents Required |

For resident Indians |

|

For NRI |

|

For OCI cardholders |

|

Source: myScheme3

Let us now take a closer look at the features and characteristics of the minor pension account:

Features And Benefits

Investors must be aware of the following features, not only to invest efficiently in the NPS Vatsalya scheme but also to understand the NPS Vatsalya benefits.

1. NPS For Minors: Under the NPS Vatsalya scheme, parents or guardians can begin building the retirement corpus for a minor. Such an early beginning gives a significant head start in the investment journey. The NPS Vatsalya eligibility criteria that must be met to invest in this asset are discussed here.

- A minor citizen of India who has not reached 18 years of age.

- The account may be opened in the minor's name by natural or legal guardians.

- If the guardian is court-appointed, a copy of the court order and Know Your Customer (KYC) is required.

- The parent manages the account for the minor.

2. Asset Mix: The corpus of the NPS Vatsalya scheme is invested in debt, equity, and other assets. There are three variants of the NPS Vatsalya scheme, each of which maintains a different percentage allocation of equity and other lower-risk assets to meet different investor goals and risk appetite. The chart below shows this distinct composition.

NPS Vatsalya Asset Allocation Variants | Asset Allocation |

Default Choice | The default choice, when investing in NPS Vatsalya, is the Moderate Lifecycle Fund - LC-50. This fund invests 50% of its corpus in equity. |

Auto Choice | Apart from the Moderate Lifecycle Fund - LC-50, there are two other fund options.

|

Active Choice | Under this variant, parents can actively customise the allocation of funds in equity (up to 75%), government securities (up to 100%), corporate debt (up to 100%), and alternate assets (up to 5%). |

Source: npstrust.org4

3. NPS Vatsalya Minimum Deposit: The NPS Vatsalya minimum contribution is INR 1,000, resulting in a low entry barrier. Furthermore, NPS Vatsalya has no maximum limit. This makes the scheme affordable to small and big investors alike.

4. Seamless Continuity To Regular NPS: The NPS Vatsalya scheme is for minors, wherein parents and guardians can invest periodically till the child hits 18 years of age. Once the beneficiary reaches 18 years of age, they are no longer a minor, and their NPS Vatsalya account is converted into a regular NPS Tier I account. A fresh KYC within three months of hitting 18 is required. This allows investment continuity, aiding the process of long-term compounding.

5. Use Other Than Retirement: Not only for retirement, investors can withdraw a certain portion of their investments to meet other essential needs as well. 75% or more of the corpus can be used to meet educational needs, treatment of specified illness, or disability of the beneficiary. Furthermore, 25% of the contribution, excluding returns, can be withdrawn a maximum of three times till the minor turns 18, after at least 3 years from the date of opening the account.

6. NPS Vatsalya Apply Online Or Offline: Investors can start their NPS investment easily through both online and offline methods. To apply online, investors need to visit the NPS Vatsalya eNPS registration website. An offline application can be submitted by visiting any Point of Presence (PoP) registered with PFRDA. PoPs are usually banks, brokers, and so on.

7. Tax Benefits: This child variant of the NPS scheme enables guardians to claim a tax deduction of up to INR 50,000 per year under Section 80CCD(1B) of the Income Tax Act5. This deduction is in addition to the 80C exemption of up to INR 1.5 lakhs. However, such exemptions and deductions are applicable under the old tax regime alone.

The primary benefit or objective of opening this child's NPS account is to get the benefit of long-term compounding by starting early. Therefore, before investing in this asset, it is crucial to gauge its return and risk profile.

Returns And Risks

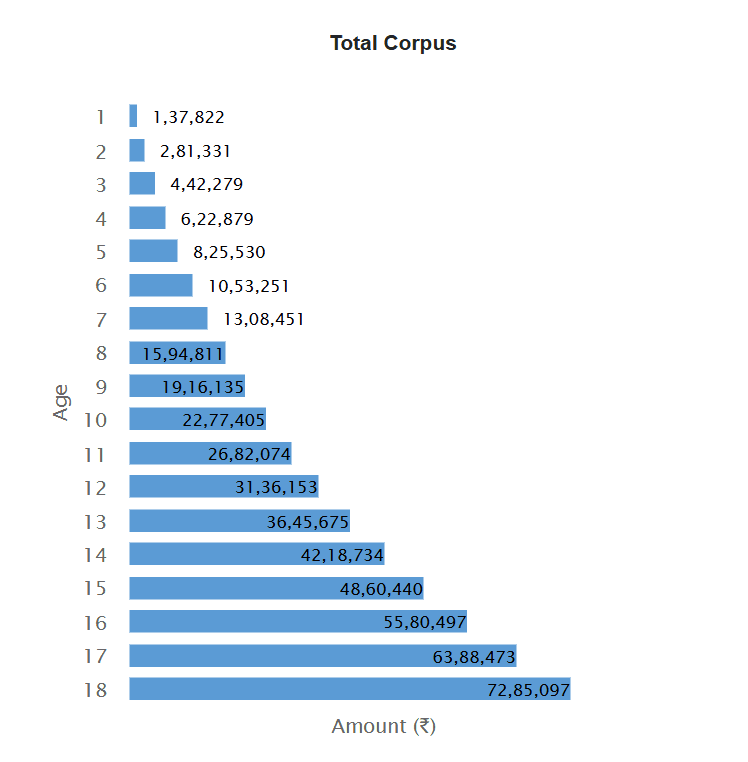

Suppose Mr and Mrs P gave birth to their child X on 3 April 2026. They begin their NPS Vatsalya investment immediately. If their monthly contribution is INR 10,000, using the official NPS Vatsalya calculator, which assumes the expected return at 12.21%, the corpus when X turns 18 stands at INR 72.85 lakh. The graph below shows the growth of the fund over the years.

However, like any asset, there are certain risks that investors must be aware of before choosing the NPS Vatsalya Scheme.

- Market Risk: Like mutual funds, NPS Vatsalys scheme invests its corpus into a range of assets, including equity. Such market-linked investments are subject to market volatility. Despite long-term growth, short-term fluctuations are inevitable.

- Liquidity Risk: NPS Vatsalya is a long-term investment, which often lacks liquidity. Apart from limited partial withdrawals for specific causes, the fund is targeted towards retirement planning.

- Annuity: If the accumulated corpus is less than or equal to INR 2.5 lakhs, at least 80% of the balance is to be used to purchase annuity, and the remaining balance can be in a lump sum6.

Like any investment medium, the unique return-risk profile and features of this asset category make it suitable to meet specific investor needs and temperament.

Should You Invest?

The NPS Vatsalya scheme is ideal for new and young families who want to take advantage of maximum compounding for their children by starting investment early. Not only the resident investors, but also the NRIs and OCI cardholders can invest in this asset. Disciplined investors, comfortable with patient long-term growth, can find this asset attractive. However, optimal investing also requires diversification. Stable growth assets like corporate bonds, debt mutual funds, high-yield FDs, and so on, can help optimise overall portfolio performance.

Grip offers a range of investment opportunities, including corporate bonds, high-yield FDs, and so on, that can offer up to 12.5% YTM. Visit Grip Invest Today!

FAQs On NPS Vatsalya

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001