Post Office PPF Plan In 2026: Interest Rate, Benefits And Withdrawal Rules

Many Indians are looking for safe, reliable and effective ways to enhance their savings over time. Of government-backed savings schemes, the Post Office PPF is considered by many as the most secure option for long-term savings. It provides an attractive return on investment with a high degree of tax advantage and with complete capital security.

What Is A Post Office PPF Plan?

PPF stands for Public Provident Fund India and is a long-term government-sponsored savings programme available at any post office or bank in India. Under PPF, the government backs your investment so that your capital will remain safe for a long time. In addition, you make regular contributions and accrue interest at an annual rate. Therefore, your money grows over time.

The PPF Scheme encourages individuals to save on a consistent basis, with a stipulation requiring the depositor to maintain their investment for a specified period of time. Thereby providing financial discipline while allowing for a consistent rate of growth.

The continuing appeal of the Post Office PPF to risk-averse investors has made it attractive to so-called conservative investors who place a premium on the safety of their principal versus chasing greater returns by taking on greater risks.

PPF Interest Rate And Returns

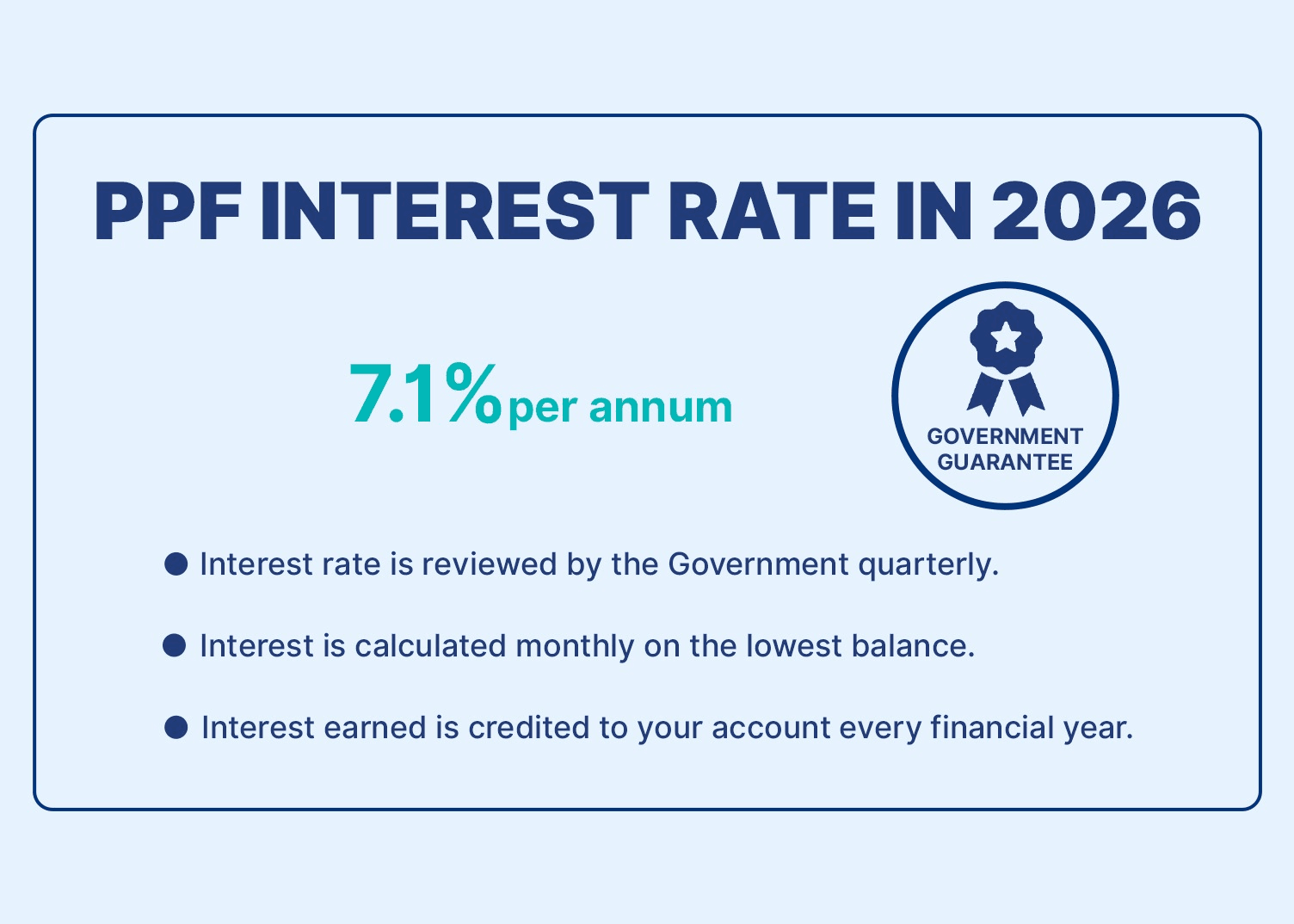

As of 2026, the post Office PPF will have an interest rate of 7.1% per annum. While the rate of interest is typically reviewed by the government quarterly, it has remained unchanged from previous reviews. The interest you receive from your post Office PPF is calculated each month on your lowest balance. Each financial year, the interest earned will be credited to your account.

The compounding effect can greatly increase how much your money will grow over an extended time period. Even a small amount of regular deposits can provide a large amount of money at the end of the term due to frequent deposits along with compound interest.

Hypothetical Example:

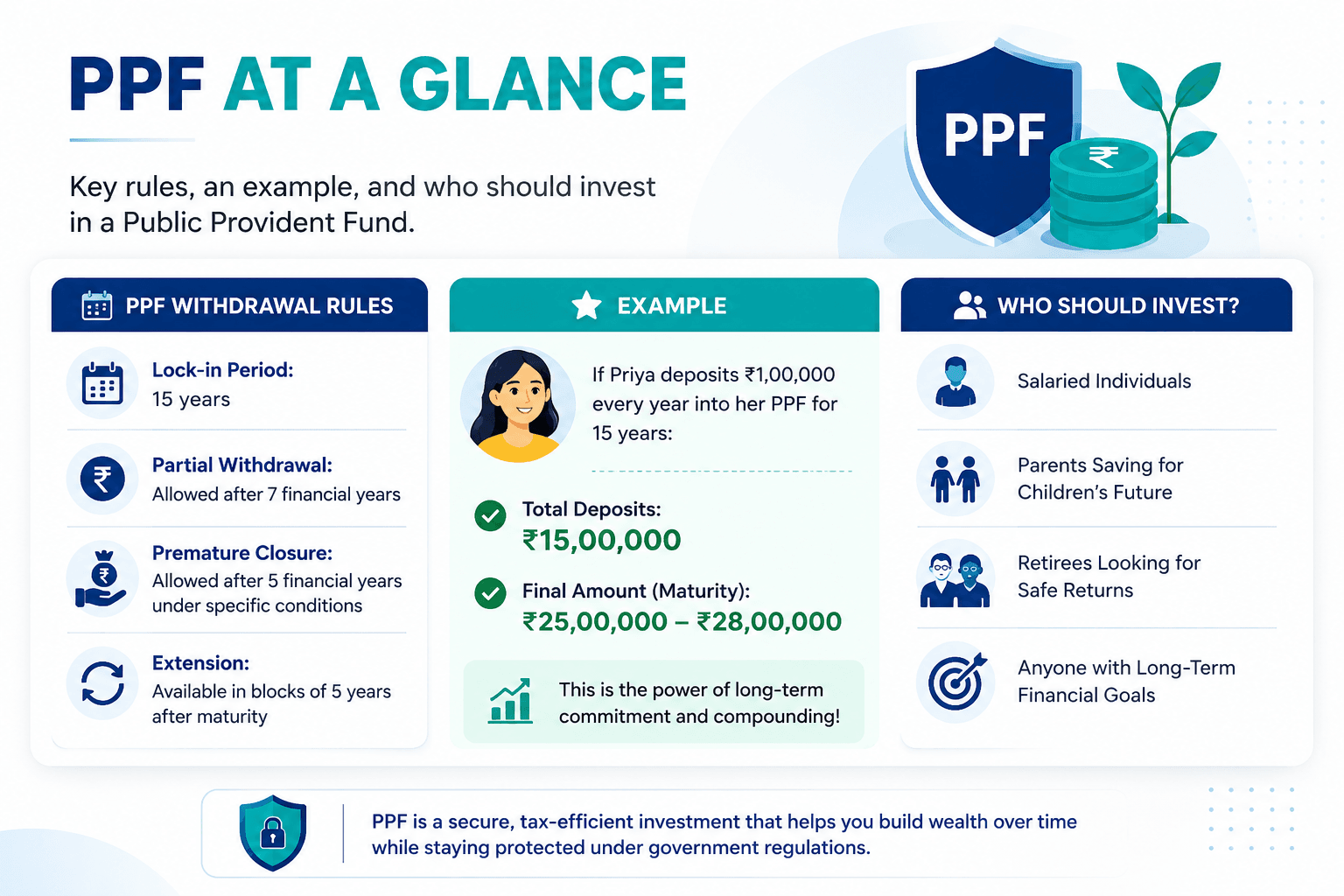

Example: If Priya deposits Rs. 1,00,000 every year into her PPF for 15 years, when she makes her final deposit, her total deposits will be Rs. 15,00,000. Since her money will earn compound interest over the entire time frame, her final amount will be Rs. 25,00,000 - Rs. 28,00,000. This is an illustration of how powerful long-term commitment can be in the PPF scheme.

To see personalized estimates based on the amount of money deposited and the length of time the money is held, you can use one of the many PPF calculators available on various financial websites.

PPF Eligibility And Investment Rules

Anyone who is a resident Indian (including salaried employees, self-employed individuals and pensioners) may apply for and open a PPF account at a post office or bank. A parent or guardian may open an account for a minor child. NRIs may not open new accounts but can continue to maintain their current accounts until they reach maturity.

The basic rules for a Public Provident Fund account are:

1. A minimum of INR 500 must be deposited per year.

2. There is a maximum investment limit of INR 1,50,000 per financial year.

3. You may make deposits in a bulk or spread them out equally throughout the year.

4. Deposits made by the 5th of each month will maximize the amount of interest you will earn that month.

You can open an account at any post office or any bank branch that is authorised to sell PPF. Many banks and India Post allow accounts to be managed online, making it even easier. You will have nominating rights on your PPF account, which will help make sure the funds go to your heirs when you die.

PPF Tax Benefits

The tax advantages associated with a Public Provident Fund account are some of the greatest aspects of the plan.

- They are styled EEE, meaning the investment contributions are deductible, the interest earned during the period of investment is tax-free, and the amount received at maturity is also tax-free.

- You may deduct up to INR 1,50,000 from your gross income under Section 80C of the Income Tax Act.

- The deduction significantly lowers your taxable income on an annual basis. In addition, there is no TDS on either the interest paid or on the proceeds from the PPF account at maturity, which makes it more hassle-free.

This makes it easy to understand why the PPF account is a good investment for the average middle-class person looking to save money on taxes while creating long-term wealth.

PPF Withdrawal Rules

The Public Provident Fund (PPF) has a duration of 15 years from the end of the fiscal year when you established the PPF. You can then withdraw your money in its entirety, or you can continue with a new 5-year term.

In spite of this extended period of inactivity, the rules surrounding withdrawals from the PPF allow for flexibility:

- You may not make withdrawals during the first six years.

- Beginning in year 7, you may make a partial withdrawal as defined by the following: You may make one withdrawal per year using whichever of the following is the lesser of the two amounts: either 50% of your balance from the end of the fourth year preceding the most recent year, or 50% of the balance from the end of the most recent year.

- If you are experiencing a situation where you need to access funds, you may close the account early; however, you will incur a small penalty fee if you decide to withdraw funds after five (5) years, but only in specific circumstances, such as a serious illness or a need for funds for education.

- Upon maturity of your PPF account, you may continue to keep your PPF account active with compounded interest accrued until maturity without depositing additional funds. You may also continue to contribute additional funds during the 5-year extension of your account.

The PPF withdrawal rules maintain the discipline to save, while providing necessary liquidity in case of emergencies such as Amit’s emergency withdrawal in year 7, based on the computed PPF balance.

Using these rules provides a cushion of comfort for the saver by maintaining their savings habit overall, while allowing them access to their funds in case of an emergency.

PPF vs Other Investments

In terms of risk and return, the post office PPF plan is probably best known as the safest investment that has the highest potential for returns, and that is also the most tax-efficient form of savings.

PPF vs FD vs Bonds vs Mutual Funds

Feature | PPF Scheme | Bank FD | Government Bonds | Equity Mutual Funds |

| Safety | Government guaranteed | High (DICGC insured) | High | Market-linked |

| Returns (approx) | 7.1% tax-free | 6-8% taxable | Around 7% | Higher but volatile |

| Lock-in | 15 years | Flexible | Varies | No lock-in |

| Tax Benefits | Tax-free | Taxable interest | Varies | LTCG after 1 year |

| Liquidity | Limited | Better | Moderate | High |

PPF vs FD is a standard comparison, and both have their place in the investment world. FDs are better when you need immediate access to cash; PPF has a large tax advantage, and post-tax return differences should be minimal over the long term compared to FDs. When choosing between FDs or PPF, consider your liquidity requirements and comfort level with risk.

Conclusion

The post office PPF plan will continue to be a keystone in making sound savings decisions in 2026. This plan provides guaranteed returns, tax-free income, and government security, which makes it appropriate for the majority of families. Whether you are saving for retirement, children's education or an emergency, by saving consistently in PPF, you can achieve the desired result in the long run. Start early, save consistently and allow compounding to take care of the rest. To learn more about investments and retirement planning, sign up for Grip Invest today. Grip offers corporate bonds and other fixed-income investment options with yields up to 12.5%.

FAQs On Post Office PPF

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001