RBI Updates Rules For Basic Savings Bank Deposit Accounts: Key Changes And What It Means For You

Introduction: RBI Revamps BSBD Account Rules For Better Accessibility

In a major policy change to enhance financial inclusion and facilitate customers, the Reserve Bank of India (RBI) has decided to modify the regulation relating to Basic Savings Bank Deposit (BSBD) accounts.

The new RBI updates rules for basic savings bank deposit accounts will come into effect from 1st April 2026, and from then on, all banks in the country will have to apply this policy in order to provide major improvements to this zero balance accounts feature banking facility.

With the RBI updating rules for basic savings bank deposit accounts, Indians in millions, from rural to digital savings, a better, fairer, and friendlier banking experience is what BSBD account rules 2026 have to offer.

What Is A Basic Savings Bank Deposit (BSDB) Account?

Basic Savings Bank Deposit (BSBD) Account: This is a type of Savings Account designed to provide basic services to people with little to no charge, and without maintaining a minimum balance. The Basic Savings Bank Deposit account was initially conceived as a means of achieving financial inclusion and was intended to replace the "No Frills" account.

Why “BSBD” Accounts Matter

- They eliminate costs as a constraint to banking accessibility.

- It enables basic transactions at low costs.

- They assist in bringing unbanked and underbanked people into the formal banking system.

Conventional BSBD savings accounts offered free withdrawals, cash deposits, and electronic credits; however, the 2026 changes reflect the evolution of these traditional offerings.

Overview Of The New RBI BSDB Account Rules

These new rules for BSBD accounts are now included in a set of seven amendment directions issued by the RBI in December 2025. Basic savings bank deposit account RBI changes have strengthened the BSBD accounts system in some significant ways under the new rules of accounts.

Here is what is new in RBI updates rules for basic savings bank deposit accounts-

- Minimum Balance Required: There are no charges or requirements for a minimum balance for opening or maintaining the BSBD account.

- Obligatory free basic services: Basic banking services must be offered free of charge.

- Extending digital access: Internet and mobile banking services must be provided free of charge to customers.

- Debit/ATM facilities: An ATM cum debit card should be made available free of charge on request.

- Cheque Book Access: Banks are to provide a minimum of 25 free cheque leaves, if required.

- Publicity and Transparency: Banks must provide clear explanations of facilities in BSBD and how they differ from normal savings accounts.

- Conversion and Eligibility: Existing savings accounts can be converted to BSBD accounts within the first 7 days after the request.

- One account rule: A person can maintain only one BSBD account in all banks. He/She must provide a declaration that they have no account before opening a new one.

Extended Free Services For BSBD Account Holders

Among the most customer-friendly changes introduced by the revised rules of the BSBD account is the increased free banking services offered to deposit account holders, which are closer to those of savings account holders.

Free Services That Are to Be Expected-

- Cash Deposits and Withdrawals

- Electronic fund transfers (UPI, NEFT, IMPS)

- Free mobile and internet banking on request

- Free ATM debit card

- Free cheque book (min. 25 leaves)

- Free passbook or monthly statement

Digital Transactions Are Easier

Unlike other norms, digital transactions such as UPI/NEFT/IMPS shall not be counted toward the restricted number of withdrawals permitted each month, and thus the BSBD account would be ideal for digital-first users.

Why These Changes Matter To Everyday Savers

These changes are not merely about fine-tuning regulations; they have a direct and meaningful impact on millions of bank account holders in India.

1. Increased Financial Inclusion

Reducing costs and improving access to basic services mean more individuals, particularly in rural and lower-income areas, can access formal banking services.

2. More Transparent Banking

Banks are also supposed to make it clear what is included in a BSBD account and what fees are charged for additional services, beyond the free services offered in a basic account.

3. Better Digital Experience

With technology driving the world of modern payments to unprecedented heights, BSBD customers can take advantage of a wide range of online banking services.

4. Increased Flexibility

Users can change savings accounts to BSBD accounts. This is a great benefit for customers seeking affordable banking options.

5. Improved Consumer Protection

Banks are obliged to comply with the Fair Pricing and Consent Principles under Responsible Business Conduct.

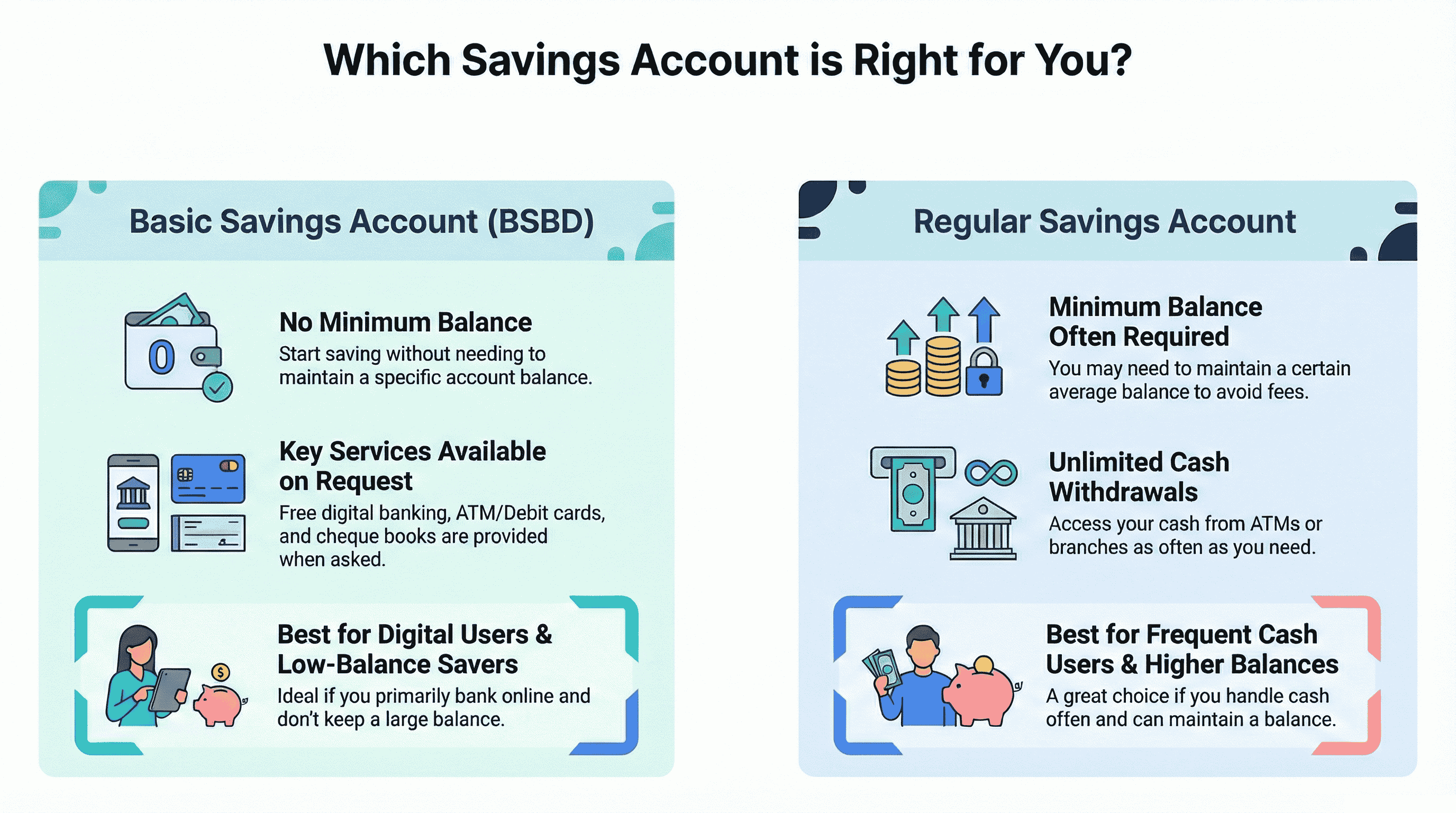

BSBD Accounts Vs Savings Accounts: Which Account Type Should You Use?

Here is how you can choose between them:

Feature | BSBD Account | Regular Savings Account |

Minimum Balance | No | Often yes |

Digital Banking | Free on request | Free |

ATM/ Debit Card | Free on request | Usually free |

Cheque Book | Free on request | Free (often automatically) |

Cash Withdrawals | Limited free (plus digital unlimited) | Usually unlimited |

Best For | Digital users, low-balance savers | Frequent cash use, higher balances |

When to Choose Regular Savings: If you make heavy withdrawals in cash, have extensive needs in benefits with bank products, or hold high balances, you will find that a regular savings account could work well for you.

Conclusion: BSBD Accounts Are Now Stronger. Your Savings Strategy Should Be Too.

The RBI updates rules for basic savings bank deposit accounts clearly signal a shift toward fairer, more accessible banking. With zero balance requirements, expanded free services, and digital transactions no longer restricted, BSBD accounts in 2026 are no longer just entry-level accounts. They are practical, modern, and genuinely useful for everyday savers.

That said, a savings account, even an improved one, is still primarily about liquidity and safety, not long-term wealth creation. Once your basic banking needs are covered through a BSBD account, the next step is to make your idle savings work harder.

This is where platforms like Grip Invest come in. While BSBD accounts help you manage money efficiently, Grip Invest helps you grow it by offering access to curated fixed-income instruments such as high-quality bonds, corporate FDs, and other regulated alternatives that aim to deliver predictable returns with transparency.

Used together, a BSBD account for everyday transactions and a disciplined investment approach through Grip Invest can help you move from simple savings to smarter financial planning—without complexity, and without locking yourself out of liquidity.

FAQs

1. What are the free services provided for the RBI's new BSBD account guidelines?

Basic banking facilities such as cash deposits/withdrawals, online Transfers, debit cards, online/Internet Banking, chequered book facilities, and Passbook/Statements are all free.

2. Are digital transactions considered withdrawals for the free limit?

No. Digital payment services such as UPI, NEFT, and IMPS are not considered while calculating your free withdrawal limit, making BSBD savings accounts more attractive to digital users.

3. What are the effects of these provisions to promote financial inclusion?

The elimination of minimum balance requirements, as well as free services, allows millions of people access to banking.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.