South Indian Bank FD Rates 2026: Latest Interest Rates And Features

In a constantly changing economy, savers want to find safe and reliable ways to grow their money. For this reason, a fixed deposit yields set returns or a fixed income with no market risk, which is what every investor wants. There are several banks that offer very competitive fixed deposit rates, and South Indian Bank is one of the few banks that offer competitive fixed deposit rates across all available tenures.

South Indian Bank's fixed deposit rates suit almost everyone, from the average working person to the retiree. This guide outlines the key factors you should consider to make an informed and confident decision when choosing a South Indian Bank fixed deposit.

Latest South Indian Bank FD Rates

South Indian Bank's fixed deposit rates are based on both the tenure and the type of customer. As a result, customers at South Indian Bank can select a fixed deposit from a wide variety of options.

Customers from the general public are offered fixed deposit rates that are attractive for 2-year terms, while senior citizens enjoy many more options and benefits within this category. Rates apply to deposits less than 3 crores; therefore, everyone can access these rates.

1. Regular Citizens

Regular citizens are offered rates on fixed deposits that are much lower at the beginning and grow with successive tenures until the 2-year period, which will produce the best fixed deposit returns. After that, the interest rates will continue to grow, but at a slightly lower rate than the previous rates.

For example, an average salaried person can put their emergency fund into a fixed deposit for 1 year and earn a great deal of interest each quarter.

2. Senior Citizens

Rates of FDs for senior citizens are better across all slabs and give higher payouts to them to enable them to get extra value for money without any difficulty. The same thing applies to the senior citizen's rate for being loyal to their banker.

For example, a senior citizen can take out a two-year fixed deposit and double his or her savings over two years, which can then be used for travel dreams.

Special Tenure Schemes

Tax-Saving FDs have a minimum five-year term in order to qualify for income tax deductions under Section 80C. There is also the advantage of a quarterly or end-of-maturity option that pays out once a quarter according to the Deposit Periods, and there are also Tax-Saving FD options for NRIs who are located somewhere other than India.

For example, a young professional can open a Tax-Saving FD account and take advantage of the deductions while still in the process of building his or her wealth.

| Tenure Bucket | General Rate Range | Senior Rate Range |

| Short (days-months) | Lower yields | Extra boost |

| Medium (1-2 years) | Peak rates | Highest payouts |

| Long (2-10 years) | Steady holds | Rewarding extras |

Features And Benefits

South Indian Bank FDs have many features and benefits that make them very attractive to the saver, and they make saving a great deal of fun.

- An individual can open an account with as little as one thousand rupees, which makes saving easy for anyone.

- The quarterly compounding creates additional wealth for an individual without the individual knowing that it is happening.

- An individual can borrow up to 100% of their deposit, which allows them to deal with emergencies without having to break the principal of the deposit, while also being able to use a portion of the funds to continue to maintain some liquidity.

- South Indian Bank FDs have the best interest rate and the best features of any FD in the country.

How To Open An FD With South Indian Bank

The process of opening an account will remain seamless, whether it is done online or through a branch.

- The technology-driven Net Banking platform allows our existing customers to book their account (via the app) immediately after identifying their desired tenure & amount.

- Our new customers will need to visit a branch, bringing in ID for account creation and then depositing cheques into their new accounts.

- App notifications will notify our customers at maturity.

Example: A busy parent uses the app (during their commute) to open the account and select the education fund payout option for their child’s education.

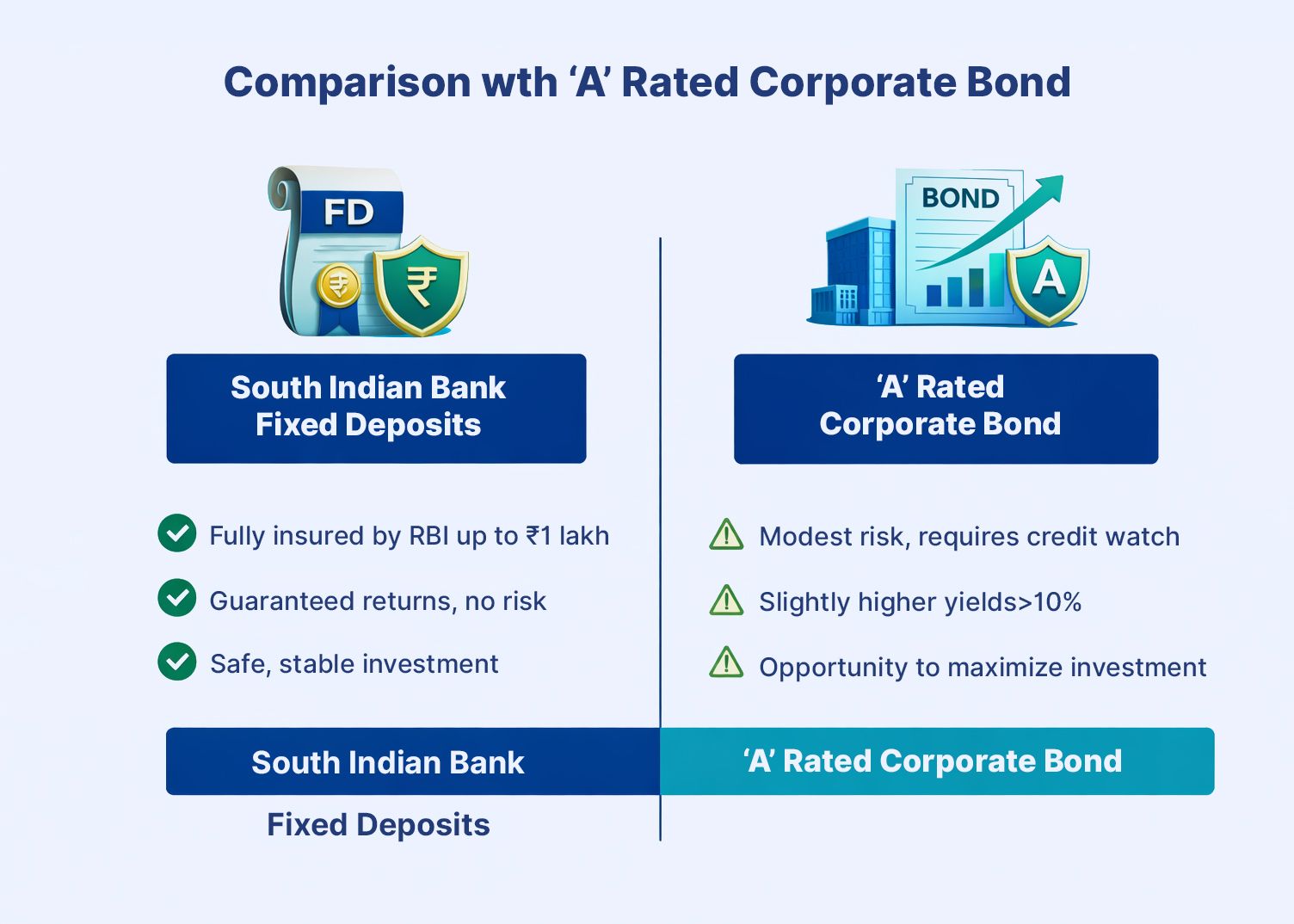

Comparison With ‘A’ Rated Corporate Bond

Compared against an “A” Rated corporate bond, our customers can rest assured that their funds in Fixed Deposit accounts are fully guaranteed by the RBI (up to Rs. 1 lac). Corporate Bonds normally trade with a slightly higher yield than 10% from respectable or solid cash-generating or ratio type companies, while Fixed Deposits are cash-generating debt covered by the RBI up to $1 lac.

If you are comfortable with taking on modest risk, you could look at purchasing an A-rated corporate bond yielding slightly higher than the SIB’s Fixed Deposits, but these companies require a regular credit watch.

If you tend to purchase physical gold, you would also have to consider that you will not have a consistent storage facility for it, as you would with digital bonds. As a scenario, the very conservative would use the Fixed Deposit for sleep at night, while the new saver would use the Corporate Bonds to achieve their goal of maximising their investment.

Beyond Basics: NRI And Tax Angles

NRE FDs give NRIs tax-free interest and a chance to repatriate savings any time. The FCNR provides an excellent opportunity to hedge currencies against both the US dollar and the euro.

The 80C deduction of qualifying tax-saving types locks savings for three or five years. However, you can partially withdraw from your NRE FD six months after opening, with some conditions attached to the withdrawal.

Renewal And Withdrawal Insights

Auto-renewal of your FD occurs at the end of the period unless you opt out. Early withdrawal incurs a penalty in most cases, but can be bypassed if you use an overdraft privilege.

Seniors should have no problem finding service branches for their needs, and you can track the status of your FD via text. This helps you avoid any surprises when your FD matures.

Exploring Corporate FDs For Better Yield Potential

While bank fixed deposits remain a dependable choice for capital safety and predictable income, some investors look beyond traditional options to enhance their fixed income returns. One such avenue is corporate fixed deposits, which are offered by financially strong companies and typically provide higher interest rates compared to bank FDs.

Through platforms like Grip Invest, investors can access curated fixed income opportunities, including corporate FDs, alongside other debt instruments. These options allow investors to compare issuers, credit profiles, tenure flexibility, and expected yields in a more transparent manner.

Corporate FDs may suit investors who:

- Are comfortable taking moderate credit risk for potentially better returns

- Want to diversify their fixed income allocation beyond bank deposits

- Are seeking flexible tenure options aligned with specific financial goals

That said, unlike bank FDs that carry deposit insurance within regulatory limits, corporate FDs are subject to issuer credit risk. Hence, investors should evaluate company fundamentals, credit ratings, and liquidity features before investing.

A balanced approach can often work well — using bank FDs for stability while selectively adding corporate FDs to enhance overall portfolio yield and diversification.

Conclusion

South Indian Bank FD rates in 2026 continue to position fixed deposits as a dependable option for investors seeking stability, predictable income, and capital protection. With flexible tenures, additional benefits for senior citizens, tax-saving variants, and NRI-friendly features, these deposits can support multiple financial goals — from building an emergency corpus to creating steady retirement income.

At the same time, fixed income investing does not have to be limited to a single product. As discussed earlier, investors can complement bank FDs with other fixed income avenues such as corporate FDs and debt instruments to improve diversification and align returns with their risk tolerance.

Ultimately, the right strategy depends on your financial priorities, liquidity requirements, and comfort with risk. Bank FDs can serve as the stable foundation of a portfolio, while selectively adding other fixed income options may help optimise yield and broaden exposure. For those looking to diversify fixed-income exposure, combining FDs with options available on Grip Invest could help create a more balanced strategy.

FAQs On South Indian FD Rates 2026

1. What are South Indian Bank's fixed deposit rates?

South Indian Bank offers a range of fixed deposit rates for both regular and senior citizens that are fairly competitive, particularly compared to other banks.

2. How secure is South Indian Bank's fixed deposit account?

Your South Indian Bank fixed deposit account is fully protected by the Reserve Bank of India (RBI). Therefore, you can have complete confidence and peace of mind when investing in South Indian Bank fixed deposit accounts.

3. What is the minimum amount I can invest in a fixed deposit?

You can invest as little as one thousand rupees into a fixed deposit account, making fixed deposits a viable investment option for small savers across all geographic regions of India.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001