Kotak Mahindra Bank FD Rates 2026: Latest Interest Rates And Returns

Conservative Investors seeking stable and predictable returns depend on Fixed Deposits due to the high-interest-rate environment. Banks offer better deposit rates when policy rates remain elevated. This offers a good opportunity to lock in higher yields for a fixed period.

If you are an investor seeking the best bank FD rates in India, checking out the Kotak Bank FD rates could prove to be useful. The Kotak Mahindra Bank is India's leading private sector bank, known for its competitive FD options across all terms, which include short-term, medium-term, and long-term. They provide the best FD rates in India. To know more about the Kotak Bank FD rates, read through this article.

Latest Kotak Bank FD Interest Rates

It is necessary to understand the tenure for your fixed deposit before you lock in your investments. The FD rates are also dependent on the period of investment.

Below are two tables that discuss the Kotak Bank FD rates for regular individuals and senior citizens.

1. Regular citizens

Term | Interest Rate ( approximately) |

| 7 to 45 days | 2.75% to 3.25% |

| 46 days to 6 months | 4% to 5.75% |

| 6 months to 1 year | 6% to 7% |

| 1 to 2 years | 7% to 7.25% |

| 3 to 5 years | 6.75% to 7% |

2. Senior citizens

| Term | Interest Rate ( approximately) |

| 6 months to 1 year | 6.5% to 7.25% |

| 1 to 2 years | 7.25% to 7.75% |

| 3 to 5 years | 7% to 7.5% |

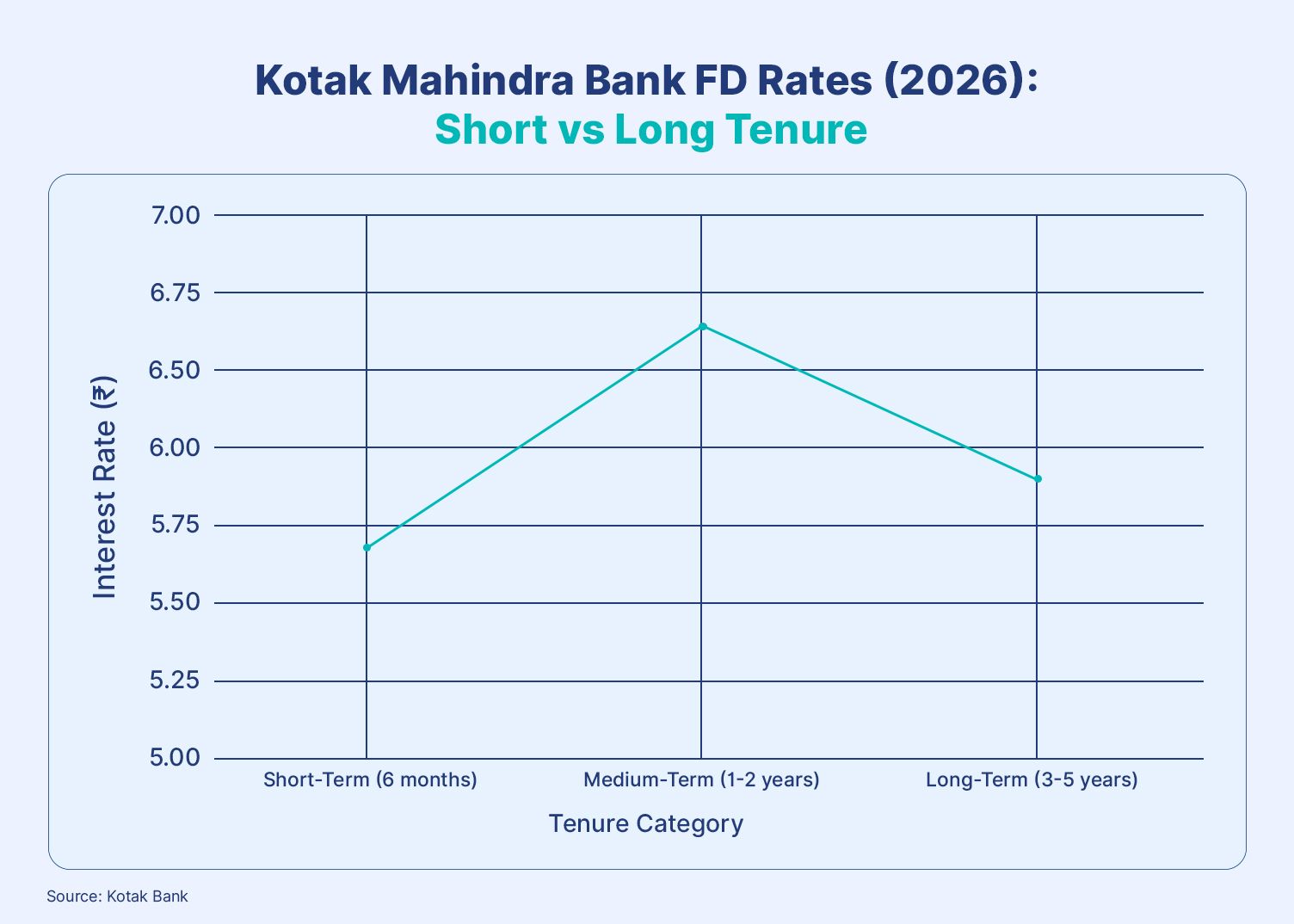

Short-term vs long-term tenures

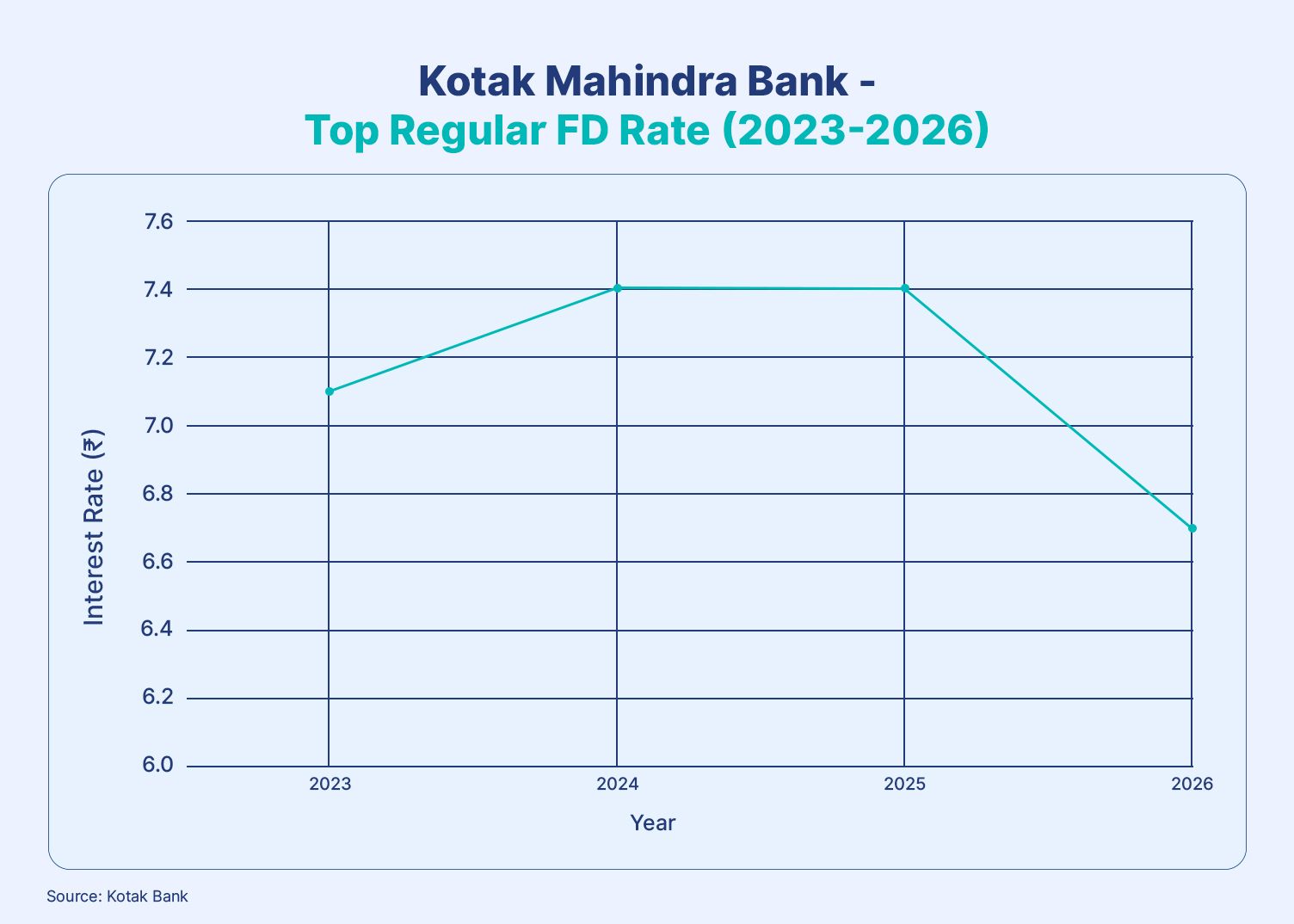

Top Kotak Bank FD Rates for 2023 to 2026

Monthly Interest on 1 Lakh in Kotak FD

To plan your cash flow better, you need to understand the return you will gain. Let us take an investment amount of INR 1,00,000 invested in a Kotak Bank Fixed Deposit.

Assuming the Kotak Bank FD rates for 2026 are around 6.70% for a time period of 1 to 2 years. Based on these assumptions, let’s calculate the annual interest and monthly equivalent income for both regular citizens and Senior citizens.

- Regular CItizens

Investment Amount: INR 1,00,000

Interest rate: 6.70%

Therefore,

Annual interest: INR 1,00,000*6.70%=INR 6,700

And,

Monthly equivalent income: INR 6,700/12= INR 558 per month ( approximately).

- Senior Citizens

Investment Amount: INR 1,00,000

Interest rate: 7.20%

Therefore,

Annual interest: INR 1,00,000*7.20% = INR 7,200

And,

Monthly equivalent income: INR 7,200/12 = INR 600 per month (approximately).

Features Of Kotak Fixed Deposits

Depending on your financial goals, the Kotak Mahindra Bank offers a wide range of fixed deposit options. These are also categorised according to time periods, which can be short-term, medium-term, or even long-term.

Below are some key features of Kotak Fixed Deposits:

1. Premature withdrawal rules

Kotak Bank FDs allow premature withdrawals but are applicable for lower interest rates, which can range from 0.5% to 1% on the original rate. This is considered a penalty for premature withdrawal. In case you keep the amount for a very short period, no interest will be paid. 5% year FDs or tax saver FDs cannot be withdrawn before the maturity date.

2. Loan against FD

You can apply for a loan against your FD at Kotak Mahindra Bank. The loan amount you apply for can typically be 85% to 90% of the FD value. The interest rate charged on such loans is 1 to 2% above the FD rate provided by the bank. Even during the loan, your FD will continue to earn interest.

3. Tax saver FD

The tax saver FD has a lock-in period of 5 years and is eligible for deduction under Section 80C. The interest earned for this tenure is taxable, and any premature withdrawals are not permitted in this case.

Kotak FD Vs Corporate FD

While banks offer fixed deposits that provide capital protection, on the other hand, corporate FDs offer higher yields alongside slightly higher risks. You should weigh safety vs return while comparing fixed income options.

| Features | Kotak Fixed Deposit | Corporate Fixed Deposit |

| Type | Private bank | Corporate issuers through investment platforms |

| Interest rates | 6% to &5 approx. | 8 % to 10% approx |

| Senior citizen benefits | Yes | No |

| Safety | High | Medium |

| Regulatory Oversight | Reserve Bank of India | Company-specific |

| Liquidity | Premature withdrawals are allowed. But applicable for the penalty | Liquidity depends on the product structure. |

| Taxation | Taxable as per the slab | Taxable as per the slab |

| Types of Investors | COservative investors | Investors looking for a higher yield |

| Loan against investment | Allowed | Not allowed |

Conclusion

Offering capital safety and predictable return, Kotak Bank FD rates are a very good option for investing in 2026. They are best suited for investors seeking capital safety. Under evolving interest rate cycles, the Kotak senior citizen FD rates remain a reliable choice of investment.

Although FDs are a convenient way for conservative investors to obtain higher yields, you must diversify your portfolio by investing in alternative fixed income options on a trusted platform such as Grip Invest. They offer curated lists of fixed-income options that focus on transparency, risk assessment, and predictable return.

To diversify your portfolio and try the best fixed-income instruments, invest with Grip.

FAQs On Kotak Bank FD Rates

1. What is the current Kotak Bank FD rate?

The current Kotak Bank FD rates for regular citizens range between 2.75% and 7.25%. For senior citizens, the rates are increased by 0.25% to 0.50% over standard rates. The rates in both cases depend on the tenure of the FD.

2. Is Kotak FD safe?

Kotak Bank FDs are considered safe. This is because the bank is regulated by the Reserve Bank of India. In addition to this, your deposits are insured upto INR 5 lakhs per depositor per bank.

3. What is the minimum deposit amount?

To open a Kotak FD, the minimum deposit amount is INR 5000. The amount may vary depending on the type of FD scheme you select.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001