Best Investment Plan For 1 Year In India: Low Risk And High Returns Options

Looking for the best investment plan for 1 year in India? You are not alone. Many investors want safe, short-term options that protect their money while still giving decent returns. Unlike long-term goals such as retirement or education planning, short-term investments are all about liquidity, safety, and stability.

When you are investing for just a year, the priority is not chasing the highest returns but preserving your capital and ensuring quick access to funds when needed. Market swings that usually balance out in the long run can hurt short-term investors if recovery time is limited. That is why the focus here is on low-risk, low-volatility instruments that deliver steady and predictable growth.

In this guide, we will explore the most reliable 1-year investment options in India, from fixed deposits and bonds to newer alternatives, so you can keep your money safe, liquid, and still growing.

Factors To Consider Before Choosing A 1-Year Investment Plan

It is important to choose low-risk investment vehicles for the short term. Consider the following factors:

A. Risk Appetite And Return Expectations

Your comfort with uncertainty shapes your options. For absolute safety, fixed deposits or sovereign-backed schemes are just right. You are open to a low risk, and short-term debt or ultra-short debt mutual funds are preferred. These offer better returns than fixed deposits, but also have proportionate risk.

B. Liquidity Needs

Liquidity is the main requirement for short-term money. In any emergency or opportunity, quick and easy access to cash becomes essential. So, investments in liquid funds or treasury bills are a common choice. Fixed maturity plans (FMPs) lock in money until maturity: a good discipline, but not much flexibility.

C. Tax Implications

Tax impact analysis carries a huge importance in shaping net returns. Here is how tax will be levied on different instruments in India:

- Fixed Deposits (FD): Annual interest income is added to the total taxable income and taxed at slab rates. If the interest surpasses INR 40,000 (INR 50,000 in case of senior citizens), TDS deductions would apply against it annually.

- Debt Mutual Funds: For debt mutual funds sold after April 2023, the holding period will not matter. Gains are always taxed according to your slab, with no indexation benefit.

- Equity-Oriented Mutual Funds: Gains within one year attract the short-term capital gains (STCG) tax of 20%. Long-term capital gains (LTCG) beyond one year are taxed at 12.5% if gains exceed INR 1.25 lakh for the assessment year.

- Gold ETFs: If held under 12 months, STCG is taxed per slab; beyond that, LTCG tax of 12.5% without indexation applies.

- Listed Debt Securities (e.g., bonds): Interest is taxed at the slab rate. For investments under 12 months, STCG at the slab rate applies; beyond 12 months, LTCG of 12.5% without indexation must be paid as tax.

- Tax-Free Bonds: Interest is tax-free, but the yield is usually lower than taxable options.

Also Read: Is Putting Rs.50k In FD for 10 Years Worth It?

Top Investment Options For A 1-Year Tenure

Some of the popular short-term investments for a holding period of 1 year are:

1. Fixed Deposits

FDs are a go-to option for capital safety and predictable returns over time. Currently, small finance banks provide attractive rates consistent with the prevailing economy at nearly 9% despite all the RBI rate cuts1.

Several banks offer rates above 8.25% on 1-year FDs from INR 3 crore and above for seniors and have higher thresholds for TDS2. Some institutions also offer higher rates around festival times.

2. Liquid Mutual Funds

These are ideal for those who prefer ready access to their funds and earn money without considering using them3. Top options like Edelweiss and Sundaram delivered ~7.2% over the last year, while others like Aditya Birla Sun Life Liquid Fund have also offered returns around 7.4%. Choose funds with strong AUM and consistent long-term performance.

3. Ultra Short Duration Funds

These yield a bit higher than liquid funds while being comparatively safe investments with low risk4. Aditya Birla Sun Life Savings Fund has returned ~8.3% for the last year. Most of these ultra-short duration funds have a 3-6 month duration and often yield returns in the range of 7.3%-8.1%.

4. Treasury Bills (T-Bills)

If ultra-safe, super liquid, and government guarantees are your top preferences for a short-term fund, go for treasury bills. As per PPFAS, the CRISIL 1-year T-Bill Index gave returns of about 6.63 as of February 20255.

5. Short-Term Corporate Bonds

Corporate bonds for the short-term offer structured exposure to investment-grade, rated corporate debt6.

The Grip Invest platform offers:

- Bonds with a 10-12% per annum yield over different tenures.

- Debt mutual funds offering returns of 7-12%.

The platform supports easy in-and-out access, with low minimums and digital convenience.

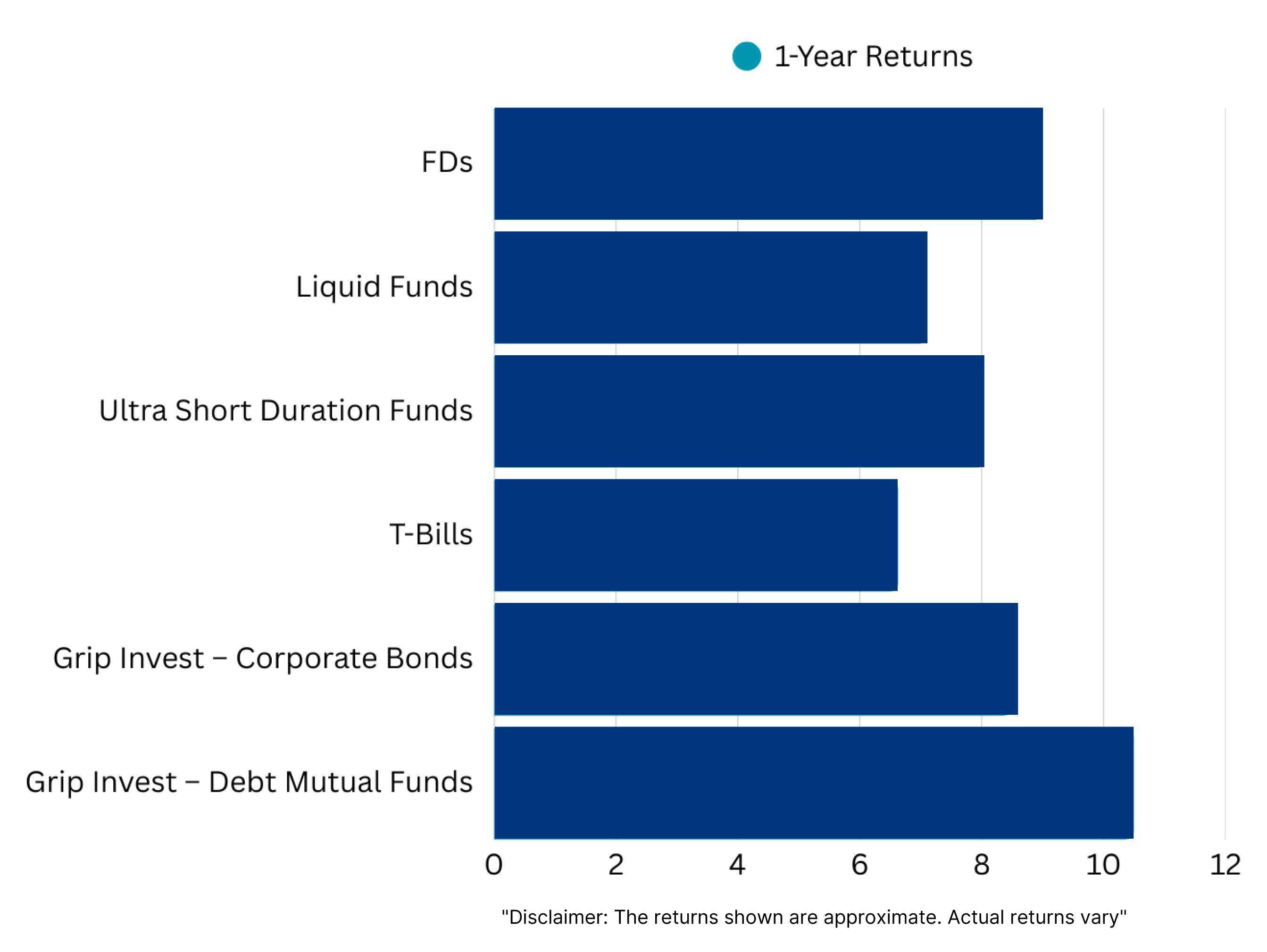

The returns from these investments vary:

Disclaimer: The returns shown are approximate. Actual returns may vary.

6. Recurring Deposits (RDs)

Recurring deposits are a disciplined savings option offered by banks and post offices, where you invest a fixed amount every month for a chosen tenure (typically between 6 months and 10 years). For a 1-year goal, recurring deposits (RDs) offer guaranteed returns at fixed rates, similar to FDs, while encouraging disciplined regular savings.

Although premature withdrawals are possible, they usually involve a small penalty. RDs are low-risk and reliable, making them a good choice for conservative investors.

7. Debt Mutual Funds

Debt mutual funds invest in fixed-income securities such as government bonds, corporate bonds, and money market instruments. They are a popular short-term investment choice because of their high liquidity and relatively low risk. For a 1-year horizon, categories like short-duration debt funds (1–3 years) and low-duration funds (6–12 months) are most relevant. Historically, many short-duration funds in India have generated returns between 6% and 8% in the past year, often outperforming traditional savings accounts or even fixed deposits (FDs). They can also be tax-efficient for investors in higher tax brackets.

8. Arbitrage Mutual Funds

Arbitrage mutual funds take advantage of price differences between the cash and derivatives markets to generate returns. They are low-volatility investments, making them suitable for conservative investors who want better returns than traditional 1-year options like savings accounts or FDs. A key benefit is that these funds are taxed as equity funds, which can be highly advantageous for investors in higher tax brackets. For short-term wealth parking, arbitrage funds provide a blend of stability, liquidity, and tax efficiency.

9. Company Deposits & Non-Convertible Debentures (NCDs)

Company fixed deposits (FDs) and non-convertible debentures (NCDs) are fixed-income instruments issued by corporates, NBFCs, and housing finance companies. They usually offer higher interest rates than bank FDs, making them attractive for investors seeking better short-term yields. However, they carry a credit risk, the possibility that the issuer may default.

To mitigate this, investors should always check the credit rating of the issuer before investing. For those willing to take a slightly higher risk, NCDs can be a rewarding 1-year investment option.

10. High-Yield Savings Accounts

Some banks and fintech platforms in India now offer high-yield savings accounts that provide interest rates above regular savings accounts, while ensuring instant liquidity. Although the returns are typically lower than debt funds or NCDs, they are ideal for investors who prioritize easy access to funds and capital safety. High-yield savings accounts work best for emergency funds or short-term goals where quick availability of money is more important than chasing higher returns.

Mistakes To Avoid In Short-term Investments

When you invest for the short-term, watch out for these mistakes:

A. Chasing The Highest Returns Without Checking Risks

It's tempting to choose that investment which has been the best performer most recently. But what goes up almost always carries hidden risks. It may be very volatile or speculative. Haphazard chasing could end with an undue burden or loss in the portfolio.

According to experts, chasing performance can mislead investors, who may buy high-performing products without understanding underlying risks. Do not allow alluring numbers to mislead you past your comfort zone with risk.

The risk, not the numbers on paper, and the investment goals should guide your choices.

B. Ignoring Taxation And Liquidity Needs

These two usually overlooked aspects can eat away at what you keep:

- Taxation: Many investors are concentrating on gross returns, not on what they will pay in taxes. In India, short-term capital gains and interests typically end up in your income tax brackets, which can reduce returns significantly. A 10% nominal return may drop below or around 4% after taxes and inflation.

- Liquidity: It's worth considering what happens in an emergency; you need access to cash in emergencies - they do not wait. But most people have locked their money in illiquid instruments or long-term commitments with no exit plans. Failure at accounting liquidity may force premature withdrawals or losses.

Conclusion

When it comes to choosing the best one-year investment plan in India, the right mix of safety, liquidity, and returns should guide your decision. Traditional favourites like fixed deposits (FDs) continue to offer reliable security, while Treasury Bills via RBI Retail Direct are emerging as a smart alternative for conservative investors.

At the same time, short-term corporate bond funds are gaining momentum, especially with stable interest rates and inflation hovering near 1.55%, offering a balanced risk–reward opportunity for those with a 12–18 month horizon. With the RBI’s evolving policy stance, interest-bearing instruments are likely to remain attractive for short-term investors in 2026.

If you’re looking to make the most of these opportunities, platforms like Grip Invest let you access SEBI-regulated, fixed-income investments with ease, helping you diversify and grow your money, one smart step at a time.

FAQs On Best 1 Year Investment Plans

1. Which is the safest investment for 1 year in India?

One-year FDs are probably the safest option. Guaranteed returns, insured for up to INR 5 lakh (for several FDs), make them one of the top choices. Treasury Bills (T-Bills) are also an alternative. These are ultra-safe state-backed government instruments with minimal default risk.

2. Can I double my money in 1 year?

Practically, doubling your money in a year would require a 100% annual return, which is virtually impossible. Short-term instruments in India, like FDs, T-Bills and debt funds, give much lower returns-usually between 5 and 12% per annum. Even equity markets, which have earned stronger long-term returns, don't usually offer this kind of gain in a year. Therefore, doubling one's money in one year is unlikely and unrealistic, to say the least.

3. Are corporate bonds a good investment in one year?

Corporate bonds or corporate bond funds are attractive for a one-year horizon, but investors need to be cautious. For example, analysts say investors having a time horizon of 12-18 months may find that these short-duration corporate bonds currently offer a reasonably balanced risk-reward mix. However, since they have credit and interest-rate risk, they typically yield a bit more than a government option. Many corporate bond mutual funds maintain their portfolio for 2-3 years. Therefore, not all exposures of one year can be aligned with the fund structure or optimal yield strategies.

References:

1. Times of India, accessed from: https://timesofindia.indiatimes.com/business/financial-literacy/savings/highest-fd-rates-despite-1-rbi-rate-cut-get-up-to-9-interest-rate-on-fixed-deposits-check-list/articleshow/122074549.cms

2. India Times, accessed from: https://www.indiatimes.com/partner/secure-your-future-on-janmashtami-explore-latest-fd-interest-rate-offers-666025.html

3. Groww, accessed from: https://groww.in/mutual-funds/category/best-liquid-mutual-funds

4. Scrip Box, accessed from: https://scripbox.com/mutual-fund/ultra-short

5. Parag Parikh Liquid Funds, accessed from: https://amc.ppfas.com/schemes/parag-parikh-liquid-fund/debt-market-insights/2025/february-2025-debt-market-insights.pdf?05032025

6. Grip Invest, accessed from: https://www.gripinvest.in/mutual-funds

7. Reuters, accessed from: https://www.reuters.com/world/india/indias-retail-inflation-slows-8-year-low-155-july-2025-08-12/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001