Zero-Based Budgeting Meaning, Examples And Key Advantages

Financial independence and successful wealth creation do not begin with investing, but with budgeting. A budget helps in planned expenditures and efficient savings, which can be directed towards investments. However, there are different methods of budgeting.

While traditional budgeting allocates funds based on past expenses, zero-based budgeting ensures active decision-making about how much and where the funds should be spent. Under this method, an investor justifies each rupee spent in a month.

The ZBB method helps avoid mystery spending and overspending, whilst enabling more informed expenditures. Most importantly, because it is a more active budgeting process, a zero-based budget makes savings more deliberate, unlike traditional budgeting, which allocates whatever is left. This blog explains zero-based budgeting in detail to help readers inculcate it in their financial planning.

What is Zero-Based Budgeting (ZBB)?

Zero-based budgeting is a financial management strategy in which all expenditures are justified from scratch for each new tenure, rather than simply revising the previous term's budget figures. Each line item, like a specific expense, saving, or debt repayment, begins with a zero base, and funds get allocated till total income minus expenses becomes zero.

For example, under traditional budgeting, if Mr K spent INR 5,000 on groceries last month, he might allocate the same INR 5,000 for the next month. However, under a personal zero-based budget, the previous year's figure would not serve as a base for the current year's allocation. In this case, Mr K decided INR 3,500 is sufficient for groceries.

A former accounting manager with Texas Instruments, named Pete Pyhrr, introduced the zero-based budgeting method between the late 1960s and early 1970s.1 As the definition suggests, a key component of the zero-based budgeting definition is its computation based on income. The total amount of money a person has serves as a crucial principle of ZBB.

The Core Principle: Income

Particularly in the personal finance application of zero-based budgeting, income is a foundational element because the goal is to allocate each rupee of income to specific purposes till income minus expenses becomes zero.

Under the ZBB method, each rupee of the total income from all sources is allocated not only to all expenses, but also to savings and debt repayments. The allocation is not based on previous budget allocations, but each line item starts from a zero base and receives active fund allocation based on individual needs.

The total income of Mr K is INR 30,000 | |

| Particulars | Allocation (INR) |

| Rent | 10,000 |

| Groceries | 5,000 |

| Transport | 2,000 |

| Phone bill | 1,000 |

| Savings | 5,000 |

| Entertainment | 2,000 |

| EMI | 2,000 |

| Emergency fund | 3,000 |

| Total allocated | 30,000 |

| Income left | 0 |

To understand the ZBB advantages and disadvantages, comparing it with the traditional budgeting method is crucial. It aids in nuanced and comprehensive analysis, required for optimal choice between the budgeting methods.

How ZBB Differs From The Way Most People Budget?

The table below compares ZBB with the conventional budgeting method.

| Particulars | Zero-Based Budgeting | Conventional Budgeting |

| Previous year's budget | It does not use previous year figures, but allocates funds from scratch. | It utilises the previous year's budget to allocate funds to various line items. |

| Savings | The individual actively allocates funds not only to expenses but also to savings. | Investors save the amount left after all expenses. |

| Flexibility | More flexible as it is more tuned to current priorities. | Less flexible as it relies more on past patterns. |

| Time effort | More time-consuming and requires more attention. | Usually faster and easier to prepare. |

| Spending habits | Can reveal unnecessary expenditures. | May enable inefficient spending to go unnoticed. |

| Investments | Savings and investment are a more active choice. | Savings and investment are passive decisions. |

Step by Step: Building A Zero Based Budget From Scratch

The zero-based budgeting steps, along with an illustrative example of Mr P is discussed here. It can aid reader understanding and help individual financial decision-making.

Step 1: List all income sources

Individuals need to calculate their total income, not only from their main profession but also from all sources. The allocation of funds to different line items would be based on this total income.

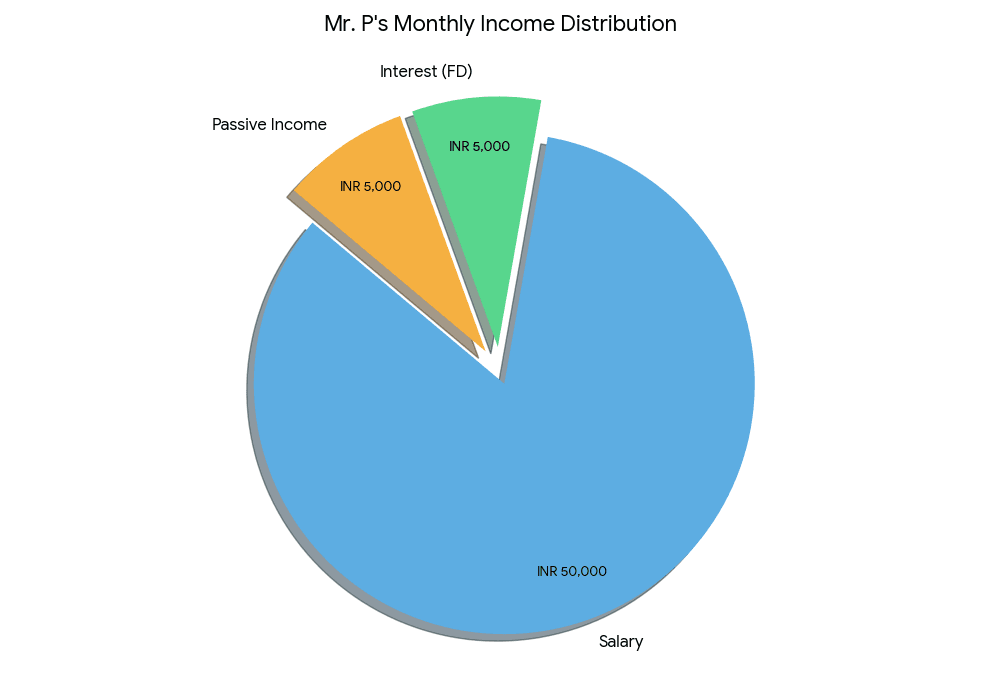

For example, Mr P earns INR 50,000 from his job, as salary, INR 5,000 as interest from a fixed deposit, and INR 5,000 from his passive income source of tutoring. Therefore, his total income stands at INR 60,000.

Step 2: List the line items

Individuals must list all the expenses, debt repayment needs, and savings needs that they want to assign funds to. Under expenses, some might be fixed, while others are variable. In the case of fixed costs, funds have to be allocated as is. For variable expenses, individuals can allocate the amount they want.

Step 3: Assign and Adjust

Individuals must not assign each rupee of the income to all the line items in the list till the total income, less allocations, becomes zero.

The table below shows the zero-based budgeting of Mr P.

The total income of Mr P is INR 60,000 | |

| Particulars | Allocation (INR) |

| Rent | 10,000 |

| Groceries | 6,000 |

| Transport | 4,000 |

| Phone bill | 1,000 |

| Investments | 10,000 |

| Entertainment | 5,000 |

| EMI | 10,000 |

| Emergency fund | 12,000 |

| Savings account | 2,000 |

| Total allocated | 60,000 |

| Income left | 0 |

However, not just for personal use, the zero-based budgeting system is used by companies as well.

ZBB In Corporate India: Companies That Use It

The zero-based budgeting system is not only used by individuals to prepare their own financial budgets, but also by companies to allocate costs and ensure optimal fiscal management. The ZBB system allows a company to maintain keen control, as they account for each and every penny that the business earns. Several companies in India, operating in the public and private sectors, have used this system for cost optimisation. For instance, Companies like Britannia Industries Ltd. and Union Carbide had adopted ZBB in 1977-78.2

However, public disclosure of companies relating to their budgeting systems is limited. Although ZBB remains a popular cost-saving budgeting tool, conglomerates often use several mechanisms in combination with one another. The emergence of other, more sophisticated financial management systems has transformed the way ZBB is used.

Grip offers a range of investment opportunities, from corporate fixed deposits to high-yield bonds that can offer up to 12.5% YTM.

Conclusion

Zero-based budgeting encourages individuals to become more intentional with their money by assigning every rupee a purpose. Unlike traditional budgeting methods that rely heavily on past spending patterns, ZBB promotes active financial decision-making, better spending discipline, and more structured savings habits.

Whether used for personal finance or business cost management, the ZBB method can help identify unnecessary expenses, improve financial clarity, and create stronger long-term financial habits. While it may require more effort and regular tracking, the increased control over income and expenses can make budgeting far more effective.

As you build smarter budgeting habits, pairing disciplined savings with reliable investment options can help strengthen your financial future. Grip offers investment opportunities across corporate FDs, bonds, and other fixed-income products designed to help investors grow wealth with greater stability.

FAQs On ZBB

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001