Best Investment Plan For Child In India: How To Build A Secure Future Step By Step

Today, raising a child in India comes with an increase in financial responsibilities. This includes healthcare, education, and lifestyles. In India, the growing cost of education is estimated to rise 8 to 12% per year, which is above the general inflation1. In other words, if the price of a course is around INR 10 Lakhs today, it will cost INR 25-30 lakhs in 10 to 15 years.

These rising costs make financial planning essential for Indian parents who want to secure a stable future for their children, rather than facing last-minute stress. By choosing the best investment plan for your child, you will not only save money but will also be able to use time to your advantage.

In India, you have multiple options for planning your child’s future, which include government schemes and market-linked investments such as mutual funds. As a parent, it is necessary to understand each option and how they work to build a goal-oriented and structured plan, instead of relying on a single product.

Key Factors To Consider Before Choosing A Child Investment Plan

A parent needs to understand and inquire about choosing the right plan before investing. Evaluating multiple plans alongside other practical factors can help align them with your goals and risk tolerance.

1. Investment Time Period

Your investment horizon depends on your child’s age. Starting early gives a longer horizon, exposing you to growth-oriented assets, while the shorter ones focus on capital preservation.

2. Tolerance to Risk

Every parent has a different risk level or comfort level while investing. Investments that are market-linked come with higher returns but are volatile, whereas fixed-income investments have lower growth but provide stability. Having an understanding of your tolerance to the level of risks can help you choose the correct mix of assets.

3. Investment Goals

Before choosing the best investment plan for your child, first you should understand your investment goals. Having defined investment goals or financial goals will help you estimate the corpus size and also choose instruments suitable for you.

4. Impact of Inflation

Inflation is a very important factor when it comes to investments. The education inflation has grown faster than the general inflation, making it crucial for parents to make a well-informed investment.

5. Liquidity of Funds

Liquidity of funds is completely your decision. Child investment plans come with lock-in periods as well as fast withdrawal. Hence, a parent needs to assess the liquidity requirements, also considering emergencies or any change in priority in the near future.

Popular Child Investment Options In India

There are multiple child investment options in India. Choosing the best investment plan for a child often depends on the parents’ financial goals and investment range.

1. Child-Specific Mutual Fund Plans

The child-specific Mutual Fund Plans reduce premature risks by encouraging long-term plans. These plans are usually used as a core growth component in a child's education investment in India.

2. PPF

A PPF offers capital safety and tax benefits as it is a government-backed scheme. It provides long lock-in periods, commonly used as a low-risk component within the best savings plan for a child.

This government scheme has been specifically designed to provide financial security for girls, offering attractive interest rates and tax advantages. It is suitable for long-term planning due to the lock-in option and works best when combined with growth assets for balanced returns.

4. Recurring Deposits and Fixed Deposits

Fixed deposits, such as bank deposits, are easy to understand and are widely used, providing predictable returns and high liquidity. But post-tax returns are lower than inflation, making these instruments better suited for short-term goals rather than long-term investments.

Low Risk and Fixed Income Options for Stability

Stability is equally important alongside building wealth using growth assets. This is where low-risk and fixed-income instruments come in, providing capital protection and predictable returns.

1. Government-backed schemes

Offering high safety and assured returns and supported by sovereign backing, instruments such as the Public Provident Fund, the Sukanya Samriddhi Yojana, and the National Savings Certificates are some plans considered among the best. They are best suited for conservative investors, securing non-negotiable future expenses.

2. Corporate deposits and bonds for predictable cash flows

Parents can get fixed interest payouts over a fixed tenure with the help of high-quality corporate bond deposits. Careful selection of these plans can help parents plan cash flow, align educational milestones, and also obtain higher returns while maintaining stability.

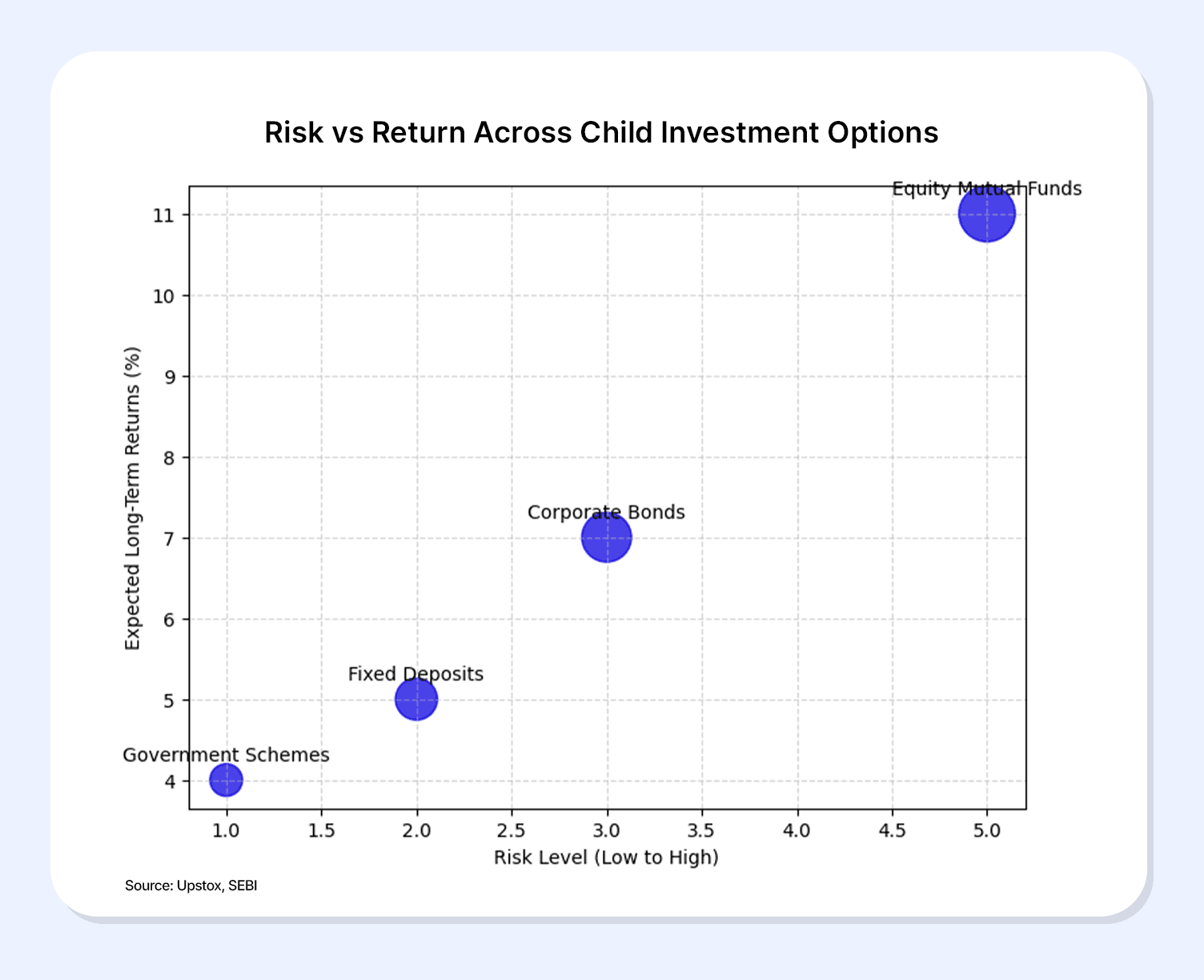

3. Risk vs return across child investment options

Building A Balanced Child Investment Strategy

The best plan for your child in India is not just a single product, but also a diversified strategy that can evolve the child’s educational and financial growth approach.

1. Combining growth assets with predictable income instruments

Parents can combat education inflation by combining growth-oriented assets, such as equity funds, to build long-term wealth. Government-backed schemes, deposits, and bonds are some fixed-income schemes that provide predictable returns, reducing volatility.

2. Gradual shift towards stability as goals approach

It is necessary to reduce risk exposure with the advancement of educational goals. Accumulated gains can be preserved by allocating a higher portion towards fixed-income options. This ensures that the funds are easily available when needed, regardless of market conditions.

Conclusion

Parents need discipline, clarity, and patience while planning a child’s future. Instead of making expensive choices, you can choose from smart and well-informed investment options. The best investment plan for your child is one that not only includes long-term growth but also includes capital protection and adaptability towards financial goals.

Diversifying your investment instruments reduces dependence on single plans, improving returns. This helps your child’s education to be funded without prior stress or hassle. Platforms like Grip Invest allow parents to strategize their investment choices by providing a curated list of fixed-income options offering transparency and predictable cash flow.

To secure your child’s future and make the best investment choices, invest with Grip Invest today!

FAQs

1. What is the safest investment plan for a child?

The safest plan is either a high-quality fixed-income instrument or a government-backed scheme. Plans that offer predictable returns and capital protection include the Sukanya Samriddhi Yojana and the Public Provident Funds.

2. Can bonds be used for child education planning?

Bonds can be used for child education investments in India. High-quality bonds provide predictable cash flow and have a fixed maturity timeline. Trusted platforms like Grip Invest provide customers with a curated list of fixed-income options.

3. How early should parents start investing for children?

Parents should start investing as early as possible. This will increase the impact of compounding and also reduce the monthly investment burden. Investment for longer periods helps with better risk management and smoother portfolio growth.

4. Are fixed income options better closer to the goal?

It is best when the fixed income option is closer to the goal. Market risks can be reduced while gradually shifting towards government schemes and bonds. This ensures that funds are available when needed the most.

References:

1. ET money, accessed from: https://www.etmoney.com/learn/personal-finance/how-to-save-invest-for-your-childs-future-in-india/?utm_

2. Upstox, accessed from: https://upstox.com/news/personal-finance/investing/small-savings-schemes-interest-rates-2025-what-ssy-nsc-kvp-and-others-investors-should-know-going-into-2026/article-186561/?utm_source=chatgpt.com

3. Cleartax, accessed from: https://cleartax.in/s/post-office-saving-schemes?utm_source=chatgpt.com

4. SEBI, accessed from: https://investor.sebi.gov.in/pdf/reference-material/corporatebonds.pdf?utm_source=chatgpt.com

5. Capital mind, accessed from: https://www.capitalmind.in/insights/estimating-longterm-equity-returns?utm_

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001